www.teitimes.com

June 2026 • Volume 19 • No 4 • Published monthly • ISSN 1757-7365

THE ENERGY INDUSTRY TIMES is published by Man in Black Media • www.mibmedia.com • Editor-in-Chief: Junior Isles • For all enquiries email: enquiries@teitimes.com

Sponsored Editorial From Hamburg to Madrid

With the addition of its PowerPods, AVK now

provides the entire power chain for a

data centre. Page 12

Following WindEurope in Madrid, TEI Times

spoke to Hitachi Energy’s Alfredo Parres

to hear the challenges facing offshore wind,

and the real progress that is being made.

Page 13

News In Brief

Fossil fuelled power

generation in structural

decline

Every OECD country in 2025 was

below its fossil-fuelled power gen-

eration peak for the rst time, indi-

cating a turning point in the transi-

tion away from fossil fuels.

Page 2

Trump anti-renewables

crusade takes effect

The Trump administration escalated

its crusade against renewable ener-

gy by stalling approvals for about

165 onshore wind projects waiting

for sign-off from the Department of

Defense.

Page 4

Chinese solar exports

double amid energy crisis

Data analysed by global energy

think-tank Ember shows that Chi-

na’s solar exports reached a record

6 in arch, double the previ-

ous month, amid high energy prices

due to the U-Israel war with Iran.

Page 5

UK smooths the way to new

green energy target for 2040

The UK government has accepted

the recommendation of its indepen-

dent Climate Change Committee to

set a legally binding goal of cutting

carbon emissions per cent by

200.

Page 7

Battery storage grows ‘at

blistering pace’

Installations of batteries that store

energy for later use surged by 48

per cent in 202 from the previous

year, according to new data from

BloombergNE.

Page 8

Energy Transition

Investment Series

TEI Times analyses ietnam’s cli-

mate pledges, electricity mi and

investment environment.

Page 14

Technology Review

Long duration energy storage is fast

emerging as the key solution to re-

duce wind curtailment, stabilise

grids, and ensure that clean energy

delivers its full value. Page 15

Advertise

advertising@teitimes.com

Subscribe

subscriptions@teitimes.com

or call +44 (0)1933 392987

The EU and the UK are cracking down on the use of Chinese components in its energy

sector, as the region looks to grow its use of renewables without jeopardising national security

by increasing dependence on foreign players. Junior Isles

Europe’s offshore wind expansion running into structural supply constraint

THE ENERGY INDUSTRY

TIMES

Final Word

When trust is broken things are

torn apart, says Junior Isles.

Page 16

The import of China-made energy in-

frastructure euipment to Europe is

coming under scrutiny, with the EU and

UK recently taking steps to block the

use of solar and wind power euipment

in projects due to security concerns.

Early last month, the European

Commission said imported inverters

used to control solar panel installa-

tions and other energy technology rep-

resented one of “the most pressing

threats” to the EU’s critical infrastruc-

ture and that any funding would be

stopped from November .

European Commission spokesper-

son Siobhan McGarry told reporters

the EU Executive has decided to take

“concrete action right now” against

the “risk of disruption of the EU’s crit-

ical infrastructure by foreign actors,”

including by “developing guidance on

restricting the use of EU funds for

projects involving inverters from

high-risk suppliers.”

uppliers from China, ussia, North

Korea and Iran are affected by the ban,

an unnamed EU ofcial told Politico,

but noted that Chinese suppliers hold

0 per cent of the global market share

of solar inverters. uawei is a market

leader in the technology.

igh-risk vendors already involved

in EU-funded projects can ask for an

eception, the EU ofcial said, and

the Commission will decide by No-

vember , whether to allow the proj-

ects to continue without restrictions

on which suppliers they can use.

ccording to carry, risks posed

by foreign interference in clean ener-

gy networks include manipulation of

“electricity production parameters”,

disruption of electricity generation

and unauthorised access to operation-

al data. This could mean a “remote

shutdown… leading to countrywide

blackouts”, she said.

Europe has taken an increasingly

restrictive approach to Chinese tech-

nology imports that it judges to be a

security risk or likely to undermine

key industrial sectors such as the car

industry.

The Commission has recently out-

lined its Industrial ccelerator ct,

which will eclude China from public

funding for other clean technologies

such as electric vehicles. eanwhile,

its cyber security act will exclude Chi-

nese companies such as uawei from

telecommunications networks and so-

lar energy systems.

In a statement, uawei said the

Continued on Page 2

Europe’s offshore wind expansion is

running into a structural supply con-

straint where the turbine market is

becoming increasingly concentrated,

says ystad Energy.

ccording to the Denmark-based

global independent research and ener-

gy intelligence company, E erno-

va, iemens amesa and estas have

historically anchored western off-

shore turbine supply, but with E

Ve rn o va h a vi n g p a us e d n ew o ff s ho r e

wind orders following a series of tech-

nical and operational setbacks, ie-

mens amesa and estas now ac-

count for virtually all turbines

available to European developers.

ystad Energy’s analysis of the off-

shore wind market outlines a sharp

increase in per-megawatt () costs,

with turbine selling prices rising by

between 40 per cent and 45 per cent

since 2020, outpacing manufacturing

cost increases of 20-25 per cent over

the same period.

“Europe’s offshore ambitions are

real, and the pipeline reects genuine

political commitment. But the mar-

ket has moved into structurally tight

territory: high demand, limited sup-

plier diversity and rising turbine

compleity. That combination gives

original euipment manufacturers

(OE) real pricing power and the

ability to be selective about which

projects get built,” said ander Baks-

joberget, Offshore ind esearch at

ystad Energy. “If Europe doesn’t

meaningfully epand estern manu-

facturing capacity or rethink how sup-

ply constraints are addressed in its

auction frameworks, it won’t deliver

its post-2030 targets at the pace or

cost the energy transition reuires, es-

pecially in the current climate that has

so much uncertainty as a result of the

iddle East conict.”

ricing pressure is most acute in the

turbine’s most comple components,

says ystad Energy. The nacelle,

which houses the generator, gearbo

and power electronics that convert

wind into electricity, sits at the centre

of current supply constraints, while

similar pressures are emerging in

blade manufacturing, driven by in-

creasing turbine sizes, longer produc-

tion cycles and the logistical demands

of transporting and installing

net-generation components.

The supply constraint is not evenly

distributed across the turbine value

chain. It is most pronounced in na-

celles and blades, where supplier con-

centration is high and substitution is

limited, while towers remain compar-

atively more eible, with a broader

supplier base and lower barriers to

entry.

ccording to ystad, the mi of tur-

bines being delivered between 2020

and 202 shows how uickly the mar-

ket has changed. Earlier years were

dominated by smaller -0 tur-

bines, while more recent deliveries

are shifting toward the larger 14-15

class. iemens amesa was rst

to move into bigger turbines, signing

contracts for its model ahead

of estas before moving into the

class, while estas’ 236-

grew in popularity from 202

onward. iemens amesa still holds

the larger overall share of deliveries,

cementing its position as the market

leader. This shift in turbine size is im-

portant context for understanding

price increases: the turbines being

built and installed today are signi-

cantly larger and more comple than

those from ve years ago, and that

compleity is reected in what OEs

can charge.

The 40-45 per cent rise in turbine

selling prices since 2020 cannot be

eplained by rising costs alone. In

2020-202, turbines were sold under

contracts that assumed relatively sta-

ble input costs, and when ination hit

hard through 202-2023, manufactur-

ers were locked into those agreements

and absorbed the losses themselves.

hen those contracts epired from

2023 onward, prices reset sharply and

the burden shifted to developers, who

now face higher turbine prices and

tighter contract terms. anufacturers

are recovering their margins on newer

deals, though protability across off-

shore divisions remains sueezed by

the costs of ramping up and scaling a

new generation of larger, more com-

ple turbines.

The key shift in the offshore turbine

market is not just the level of cost in-

ation, but how those costs are dis-

tributed across the value chain. ys-

tad Energy’s analysis models a

scenario where a 30 per cent increase

in selected input categories would

raise total manufacturing costs by

roughly per cent, reecting how

different components are eposed to

different cost drivers.

EU takes hardline against

EU takes hardline against

Chinese technology imports,

Chinese technology imports,

citing security concerns

citing security concerns

McGarry: the Commission is taking “concrete action right now”

audiovisual.ec.europa.eu

THE ENERGY INDUSTRY TIMES - JUNE 2026

2

OECD nations have reached a deni-

tive turning point, transitioning from a

historical peak in fossil fuel generation

to a sustained and structural decline,

according to recent report from UK-

based energy think-tank Ember.

Ember’s ‘Global Electricity Re-

view’ showed that record solar growth

meant clean power sources grew fast

enough to meet all new electricity

demand in 2025, thereby preventing

an increase in fossil generation, which

saw a small fall of 0.2 per cent. This

was the rst year since 2020 without

an increase in electricity generation

from fossil fuels and only the fth year

without a rise this century.

The analysis further shows OECD

fossil generation in 2025 was 19 per

cent below its peak. Since peaking in

2007, fossil fuel generation in OECD

has dropped 19 per cent (-1313 TWh),

lowering its share in the mix from 63

per cent to 48 per cent by 2025. This

shift resulted in a 28 per cent reduction

(-1477 MtCO2e) in OECD power

sector emissions. The rise in solar and

wind generation in this period (+2138

TWh) met both the fall in fossil gen-

eration (+1313 TWh) and also the rise

in electricity demand (+630 TWh) in

their entirety.

Every OECD country in 2025 was

below its fossil generation peak for

the rst time. Nearly all, 36 out of the

38, OECD countries saw fossil gen-

eration peak in 2019 or before. Tür-

kiye peaked in 2021, and Colombia

peaked in 2024. Two member states

– Iceland and Costa Rica – now oper-

ate zero-emission power systems, a

further seven maintain fossil share

below 10 per cent, while a group of

six nations remains heavily reliant on

fossil fuels for over 60 per cent of their

electricity generation.

Non-OECD fossil generation fell in

2025 as China peaks and India avoids

coal reliance.

Beyond the OECD, 2025 also

marked the rst year this century, out-

side the COVID affected 2020, in

which non-OECD fossil generation

fell, as China (-0.9 per cent) and India

(-3.3 per cent) both fell. China’s fossil

output declined as solar expanded

rapidly. India, meanwhile, is moving

towards clean energy without repli-

cating the coal heavy trajectory of

earlier industrialising economies.

The report said ambitious coal

phase-out targets, combined with rap-

id wind and solar deployment, have

allowed OECD nations to increasing-

ly decouple their electricity sectors

from fossil fuels in favour of a clean-

er power mix.

“For governments, this shift rep-

resents a strategic pivot toward ener-

gy sovereignty; by prioritising do-

mestically generated renewables,

countries are insulating themselves

from the price volatility and geopolit-

ical risks that accompany dependence

on global fossil fuel markets,” the

report stated.

The ndings came as the Interna-

tional Renewable Energy Agency

(IRENA) published a report showing

that the economics of solar and wind

energy paired with battery storage in

prime solar and wind regions deliver

round-the-clock power at lower costs

than fossil fuels.

Firm levelised costs of electricity

(‘rm costs’) for solar plus storage

range from $54-82/MWh in high-

quality resource regions, compared

with $70-85/MWh for new coal in

China and more than $100/MWh for

new gas globally.

Commenting on the report, IRENA

Director-General Francesco La Cam-

era said: “24/7 renewable power is

now cost-competitive with fossil fu-

els. The long-standing argument that

renewables lack reliability no longer

holds. Today, renewables can deliver

reliable, round-the-clock power. As

oil and gas markets remain exposed

to geopolitical shocks, including on-

going disruptions in the Strait of Hor-

muz, we must insulate our economies

with resilient renewable systems.”

Commission failed to provide “any

specic facts or technical evidence”

to back its decision.

“This restriction lacks an objective

and transparent basis, constitutes

origin-based discrimination, and

violates the principle of fair and

non-discriminatory treatment in

international trade... All suppliers

should be held to the same standards

of technical transparency and cyber

security,” Huawei said.

A report issued in late April by

Loom, a non-prot organisation

focused on economic, environmen-

tal and national security issues, said

dependence on Chinese green tech-

nology was making European coun-

tries vulnerable to cyber attacks,

trade restrictions and espionage.

The report co-authored by Mi-

chael Collins, a former deputy head

of national security strategy in the

UK Cabinet Ofce, said European

governments were failing to fully

account for such risks as they roll

out Chinese green tech in a bid to

secure energy supplies and address

climate change.

Collins told the Financial Times

that countries risked “sleepwalking

into a scenario where you’re sud-

denly confronted with a big nation-

al security problem”.

The report, co-authored by Mi-

chal Meidan, Director of the China

Energy Programme at the Oxford

Institute for Energy Studies and

based on interviews with energy

and national security experts, iden-

tied eight separate risks linked to

an over-reliance on Chinese green

technology.

Among the greatest was supply

chain disruption, according to the

authors, who argued that China was

likely to restrict supply of low-car-

bon technology and components.

Asked about the report, the foreign

ministry in Beijing said the essence

of China-EU trade relations was

“mutual benet and win-win out-

comes” and should not be “politi-

cised or subjected to an overly broad

security framing”.

Chinese ofcials dismissed con-

cerns about dependence on their

country’s green technology, say-

ing that Beijing has no intention

of using it for political advantage

and that cheap turbines, solar pan-

els and other renewable energy

products reduce the much greater

risk stemming from high carbon

emissions.

Loom’s Executive Director, Joss

Garman, said the recent fossil fuel

price shocks “should accelerate Eu-

rope’s energy transition but new

dangers arise because the cheapest

route runs so overwhelmingly

through China”.

Meanwhile, in late April, Chinese

wind turbine maker Ming Yang

Smart Energy accused the UK of

“politicisation” after the UK gov-

ernment ruled in March that Ming

Yan g cou ld no t dep lo y i ts p roduct s

in offshore projects in the country,

and rejected plans to invest £1.5

billion in manufacturing turbine

blades and other parts in the Scottish

Highlands.

Ming Yang’s Chair, Zhang Chuan-

wei, said in an interview with the

FT that the UK’s “politicisation” of

the investment would not only harm

Ming Yang but also “greatly under-

mine the sense of security Chinese

companies feel when entering the

British market”.

He said that he and other Ming

Yan g executi ves had spo ke n to th e

UK’s energy ministry, but the gov-

ernment declined to explain what

made its products a national securi-

ty threat.

Continued from Page 1

New research led by the University of

Oxford and University College Lon-

don (UCL), UK, has revealed that pol-

lution from coal red power plants is

signicantly reducing the energy out-

put of solar photovoltaic (solar PV)

installations, particularly where these

are expanding side-by-side.

The ndings, published in Nature

Sustainability, map and assess more

than 140 000 solar PV installations

worldwide using satellite data. By

combining this with atmospheric data

on air pollution, the researchers cal-

culated how much sunlight is lost and

how this reduces electricity genera-

tion. They found that aerosols – tiny

particles suspended in the air – re-

duced global solar electricity output

by 5.8 per cent in 2023. This is equiv-

alent to 111 TWh of lost energy – the

amount generated by 18 medium-

sized coal red power plants.

Crucially, these losses represent a

signicant and often overlooked

constraint on the clean energy transi-

tion. Between 2017 and 2023, new PV

installations added an average of

246.6 TWh of electricity each year,

while aerosol-related losses from ex-

isting systems reached 74.0 TWh an-

nually – equivalent to nearly one-third

of the gains from new capacity. This

highlights a previously unrecognised

interaction between fossil fuel use and

renewable energy, where emissions

from one system directly reduce the

performance of the other.

Lead author Dr Rui Song (Depart-

ment of Physics, University of Ox-

ford, and Mullard Space Science Lab-

oratory, UCL) said: “We are seeing

rapid global expansion of renewable

energy, but the effectiveness of that

transition is lower than often assumed.

As coal and solar expand in parallel,

emissions alter the radiation environ-

ment, directly undermining the per-

formance of solar generation.”

To identify the sources of these

aerosol-related losses, researchers

traced their origins and found coal

red power generation to be a major

contributor. This effect is particularly

evident in China, where solar and coal

capacity have expanded in parallel and

are often co-located. Regions with

high coal capacity aligned closely

with areas experiencing the greatest

solar PV losses.

China is the world’s largest solar

producer, and generated 793.5 TWh

of solar PV electricity in 2023 (41.5

per cent of the global total). But it also

experienced the largest losses from

aerosols, with total output reduced by

7.7 per cent. The researchers estimate

that around 29 per cent of aerosol-re-

lated solar PV losses in China come

specically from coal red power

plants. Coal plants emit ne pollution

particles that scatter and absorb sun-

light, reducing the amount that reach-

es nearby solar panels. As a result, the

panels generate less electricity than

they otherwise could.

Interestingly, China was also found

to be the only major region showing

a sustained improvement. Aerosol-re-

lated solar PV losses declined by an

average of 0.96 TWh per year (-1.4

per cent annually) between 2013 and

2023. This is likely due to stricter

emission standards and widespread

adoption of ultra-low-emission tech-

nologies within coal red power

plants, rather than a reduction in coal

capacity itself.

Co-author Dr Chenchen Huang

(University of Bath) said: “Our nd-

ings send a clear warning to the Sus-

tainable Development Goals: over-

looking pollution-induced solar

energy losses can lead to a systematic

overestimation of renewable energy

output by governments, businesses

and the broader community. To stay

on track, policies must account for this

hidden drag and shift fossil-fuel sub-

sidies away from coal.”

The Global Renewables Alliance

(GRA) has announced its 2026 corpo-

rate partners, bringing together leading

companies from across the renewable

energy value chain at a critical moment

for the global energy transition. As

countries and businesses face contin-

ued energy insecurity, price volatility

and growing pressure on competitive-

ness, the partnership underlines the

urgent need to accelerate the deploy-

ment of renewable power, grids and

storage.

This year’s partners include Fortes-

cue, Iberdrola, Arup, EDP, Hitachi,

Octopus Energy Generation, Ørsted,

SSE, SUNOTEC, and Vestas.

Together, these companies represent

a broad cross-section of the global

energy ecosystem, including develop-

ers, utilities, technology providers,

manufacturers, investors, advisors,

and major energy buyers. By partner-

ing with GRA, they contribute indus-

try expertise and strengthen the pri-

vate sector voice in support of tripling

global renewable energy capacity by

2030.

“Energy has become a dening issue

for economic stability and competi-

tiveness,” said Bruce Douglas, CEO

of the Global Renewables Alliance.

“The companies partnering with GRA

this year are demonstrating that re-

newables, combined with grids, stor-

age and electrication, are not only

the fastest and cheapest route to de-

carbonisation, but the foundation of a

secure and resilient energy system.

Turning ambition into implementa-

tion is now the priority.”

Across industries, partners high-

lighted the growing role of renew-

ables in addressing today’s energy

challenges.

Andrew Forrest, Executive Chair-

man and Founder at Fortescue, said:

“Volatile fossil fuel prices are a hand-

brake on global growth. Nations and

industries cannot build prosperity on

fuels that swing wildly in cost and

security. The only real pathway for-

ward is clear – replace fossil fuels with

abundant, predictable renewable en-

ergy. Fortescue is proving that heavy

industry can be decarbonised now, not

decades from now.”

Gonzalo Sáenz de Miera, Director

of Climate Change and Alliances at

Iberdrola, said: “Electrication is at

the heart of the response to today’s

security and competitiveness chal-

lenges, stemming from the continued

dependence of our energy model on

fossil fuels… Through our partner-

ship with the Global Renewables Al-

liance, we are joining forces with key

partners to accelerate electrication

worldwide and deliver meaningful

benets across society.”

Through their partnership with

GRA, the companies will share prac-

tical business experience and demon-

strate how renewable energy is al-

ready delivering tangible benets for

businesses and economies.

Headline News

Corporations join Global Renewables Alliance to strengthen energy security

Fossil fuelled power generation

Fossil fuelled power generation

in structural decline

in structural decline

Every OECD country in 2025 was below its fossil fuelled power generation peak for the rst

time, indicating a turning point in the transition away from fossil fuels. Junior Isles

Coal pollution reduces solar power output, study nds

Photo by www.pexels.com

THE ENERGY INDUSTRY TIMES - JUNE 2026

3

MESSE MÜNCHEN, GERMANY

—

The International Exhibition

for Energy Management and

Integrated Energy Solutions

n Ready for a 24/7 renewable energy supply: infrastructure for modern grids

n Efficiency through digitalization: intelligent grid monitoring and

management

n Balanced grids: unlocking and leveraging flexibility potential

n Industry meeting point: 100,000+ energy experts and

around 2,800 exhibitors at four parallel exhibitions

www.EM-Power.eu

SCAN FOR

ALL INFO

EU

P

VSE

C

43rd European

Photovoltaic Solar Energ

y

Conference and Exhibition

14 18

Sep

tember

WTC

World Trade Center

Rotterdam

The Netherlands

EUPVSEC.ORG

MEET THE GLOBAL PV COMMUNITY IN ROTTERDAM

The EU PVSEC is the leading global event for photovoltaics, combining a world-

class scientic conference with a dynamic industry exhibition. Researchers,

manufacturers and innovators come together to shape the future of solar energy.

Why participate?

• Showcase your innovations to an international PV audience

• Connect with industry leaders and decision-makers

• Increase your brand visibility in the growing solar market

Join the EU PVSEC 2026 in Rotterdam.

17, 18 & 19 November 2026

Köln Messe, Cologne, Germany

100% focused Exhibition on

Next Generation Power Transmission

and Distribution Technologies

• FREE ADMISSION to Qualified Visitors only – TSOs,

DSOs and Utilities – No Public Admission

www.powertranstech.com

4

TECHNOLOGY

PRESENTATION

STAGES

3

INTENSIVE

DAYS

220+

EXHIBITORS

2000+

VISITORS

THE ENERGY INDUSTRY TIMES - JUNE 2026

7

Europe News

Janet Wood

A Swiss parliamentary commission

has narrowly backed allowing the con-

struction of new nuclear power plants

in the country, endorsing an amend-

ment to the nuclear energy law by 13

votes to 12. It rejected proposals to

mandate state funding.

The Council of States has already

voted to lift the current ban. The Na-

tional Council will decide next,

though the nal word is likely to rest

with voters.

Opponents had sought additional

conditions, including a detailed

waste-disposal strategy, stronger pri-

oritisation of renewables and a revised

electricity supply plan. A proposal to

limit approval to fourth-generation

reactors also failed. A majority of the

commission argued that energy policy

should remain technologically neutral

and keep all options open. Some ar-

gued that lifting the ban would under-

mine planning certainty for renew-

ables and expose the public sector to

substantial nancial risks.

A separate proposal, the Stop Black-

out initiative, also seeks to lift the

current ban on nuclear new-build.

Since it published its 2017 Energy

Strategy, Switzerland has prohibited

new nuclear plants, while allowing

existing ones to operate as long as they

are safe. Swiss-based utility Axpo es-

timates that existing Swiss nuclear

plants, Gösgen and Leibstadt, can con-

tinue operating for another 80 years,

but under current plans Gösgen will be

disconnected from the grid by 2029

unless a new decision is made.

The discussion comes as Thomas

Sieber, Chair of Axpo, called for three

to four gas red power plants to be

added to Switzerland’s mix of hydro-

power and other renewables alongside

nuclear. e said gas red power plants

have major advantages because they

can be built relatively quickly and

bring eibility to the system.

“This gives us time to expand other

capacities and, from an economic per-

spective, is also the most cost-effec-

tive option for winter electricity in the

next few years or even decades,” said

Sieber.

Sieber also spoke out in favour of

focusing funding more on winter pow-

er and promoting the expansion of wind

power. Switzerland must act now to be

able to guarantee sufcient winter elec-

tricity and security of supply by 2050.

Electricity prices are likely to decline

in the medium term. More and more

renewable energies are coming into the

system worldwide, which have a

price-dampening effect, said Sieber,

who will relinquish his role as Axpo

Chair at the end of May.

eanwhile, po has ofcially

opened its largest solar PV array in

northwestern Spain. The Vilecha facil-

ity comprises four photovoltaic plants

with a combined capacity of 200 MW.

Germany has announced plans to join

a new Important Project of Common

European Interest (IPCEI) on innova-

tive nuclear technologies, making

fusion energy a strategic priority

alongside EU partners, while the gov-

ernment has pledged over €2 billion

for research and pilot projects to 2029.

The new IPCEI aims to bring togeth-

er research institutions, start-ups and

industry across Europe, with project

launches targeted for 2027.

Fusion is being supported despite still

being in the experimental stage. Euro-

pean fusion companies and industry

groups recently called for greater pub-

lic support of private sector projects

and a dedicated regulatory framework

distinct from that governing nuclear

ssion, in an open letter to the EU warn-

ing that Europe must “seize the

opportunity” or risk falling behind

countries such as the US, China, Japan

and Canada.

The US attracted more than 70 per

cent of global private fusion funding

last year, with deals worth $2.6 billion,

while Europe accounted for about $600

million in venture capital investment

during the same period. Europe lacks

large government-backed pro-

grammes, with the exceptions of the

UK and Germany.

Mark Cupta, a fusion investor at ven-

ture capital rm relude entures, said

that as start-ups moved from laborato-

ry experiments towards commer-

cial-scale devices, companies would

require “at least an order of magnitude

more capital”.

HSCALE, the hyperscale data centre

rm backed by Bain Capital, has an-

nounced the nancial closure of its

second large-scale data centre campus

in Settimo, Milan, Italy. The transac-

tion brings HSCALE’s total commit-

ted power capacity in the Milan met-

ropolitan area to 250 MW, with

ready-for-service dates in 2028.

The combined Milan investment rep-

resents more than €2 billion of capital

deployment in the region, where

pre-construction and procurement ac-

tivities are already underway. The

company said all major hyperscalers

are already present and growing in this

area, making it a primary deployment

zone for cloud infrastructure in South-

ern Europe.

Oliver Schiebel, HSCALE Chief

Executive, said: “Milan is one of the

strongest hyperscale markets in Eu-

rope and we are committing around

€2 billion to this region because we

understand what the market needs,

and are serious about its growth po-

tential. Our team closed the second

site, secured the power and is already

progressing through pre-construc-

tion, ensuring we deliver real capaci-

ty, as fast as possible.”

HSCALE’s energy strategy in Milan

is designed around a diversied supply

mix, with nearly 50 per cent of power

sourced from renewable generation

including solar, wind and hydroelec-

tric. It has a ‘structural partnership’

with Aquila Clean Energy, which it

says provides integrated access to

clean energy supplies rather than rely-

ing solely on standard power purchase

agreements.

Ocean Winds (OW) has started elec-

tricity production at its 30 MW Éoli-

ennes Flottantes du Golfe du Lion

(EL) oating offshore wind farm.

The pilot wind farm, 16 km off the

coast, aims to demonstrate the viabil-

ity of oating offshore wind develop-

ment and construction

Marc Hirt, Country Manager for

France at Ocean Winds, said: ”The

start of electricity production for

EFGL is an important milestone for

France’s energy sovereignty and for

oating wind more broadly.”

Meanwhile Nexans, RTE and Su-

perGrid Institute have announced the

launch of RHODÉ (Raccordement

HVDC Offshore Distant Électrique),

a collaborative project to develop

oating DC electrical connections

for large-scale offshore wind farms

installed in deep waters, far from the

coast.

The group said large-scale deploy-

ment of offshore wind is potentially

leading to the development of sites

located at depths greater than 100 m

and several tens of kilometres from

the coastline. Under these conditions,

traditional solutions with ed bot-

tom substations may reach their tech-

nical and economic limits. It said

RHODÉ forms the missing link be-

tween research projects already un-

derway and the industrial realisation

phase of the rst 320 k or 2 k

oating DC connections, envis-

aged from 2040 onwards.

Janet Wood

The UK government has accepted the

recommendation of its independent

Climate Change Committee to set a

legally binding goal of cutting carbon

emissions 87 per cent by 2040.

The decision comes as the govern-

ment announced reforms that will give

Parliament the authority to approve

critical energy schemes and protect

infrastructure projects from judicial

review.

The proposal would allow Parlia-

ment to designate and approve the

most important clean energy projects

as being of ‘Critical National Impor-

tance’ (CNI), reducing the exposure

from judicial review on all but human

rights grounds.

or all other nationally signicant

infrastructure – including transport and

water projects – the government will

introduce a ed legal challenge win-

dow, at the end of which the planning

consent could be updated to address

any legitimate issues. Courts would

refuse permission for a judicial review

on any issues not brought up during the

consenting period or in the challenge

window. The government is also ex-

pected to allow promoters of smaller

energy projects to apply directly to the

Planning Inspectorate, to support fast-

er decision-making on generation and

transmission.

A Treasury spokesperson said: “For

too long, vital infrastructure delivery

has been delayed by judicial reviews

of projects the country needs. The

Chancellor won’t stand for it any lon-

ger and is bringing forward bold

changes to support delivery.”

The government has also recently

made changes that would help offshore

wind developers. Until now, develop-

ers faced strict limits on the types of

environmental compensation they

could offer. The new rules open up a

wider range of options.

Marine Minister Emma Hardy said:

“Offshore wind power is a key driver

of our mission to make Britain energy

secure and tackle the climate crisis.

As we build the clean energy infra-

structure our country needs, these

reforms mean that we can also deliver

real, lasting benets for nature, from

restoring native oyster beds to pro-

tecting seabird colonies for future

generations.”

Meanwhile Schroders Greencoat and

Carlton Power have reached Final In-

vestment Decision (FID) on the 30

MW Barrow Green Hydrogen Project

in Cumbria.

The project, which is being delivered

by Green Hydrogen Energy Company

(GHECO) saw the signing of a Low

Carbon Hydrogen Agreement with the

UK government in June 2025, follow-

ing the government’s rst ydrogen

Allocation Round. GHECO is target-

ing a 200 MW portfolio of green hy-

drogen projects in the UK by 2030.

Kristian Høeg Madsen, Co-Head of

Hydrogen Investments at Schroders

reencoat, said: “e have signicant

ambitions to grow the GHECO plat-

form – reaching Final Investment De-

cision on Barrow is therefore a key

milestone for Schroders Greencoat, as

well as the UK’s emerging hydrogen

economy.”

UK smooths the way

UK smooths the way

to new green energy

to new green energy

target for 2040

target for 2040

Two more data centres totalling

250 MW planned for Milan area

Germany backs fusion as industry calls for EC support

Floating wind plant starts generation

n Permitting and nature protection rules reformed

n Final investment decision on green hydrogen plant

Switzerland moves closer to new

nuclear build

n Commission joins voices in favour n Axpo chief calls for gas plants in addition

Photo by Pexels.com

Ve st a s h a s w o n a 1 86 M W t u rb i ne

order from EDF Power Solutions

North America for the Forêt Domani-

ale Wind Project. The order includes

28 EnVentus V162-6.2 MW wind tur-

bines and 2 EnVentus V162-6.0 MW

along with a 10-year service agree-

ment. Turbine delivery is expected in

Q2 2027, with commissioning expect-

ed in Q4 2027. This is the third project

that EDF has secured through Hy-

dro-Québec’s call for tenders.

In addition, Equinor, through its

subsidiary Rio Energy, acquired the

Esquina do Vento wind project from

Ve st a s. T h e 2 30 M W pr o je c t i s l oc a t-

ed in the state of Rio Grande do

Norte in northeast Brazil. Addition-

ally, Equinor entered into a wind tur-

bine supply agreement with Vestas

for the same project. As per the sup-

ply agreement, Vestas will supply 51

V163-4.5 MW turbines, with instal-

lation scheduled to commence in

March 2027.

Wärtsilä will supply an off-grid pow-

er solution for a new data centre facil-

ity under construction in Texas, USA.

The 790 MW power plant will operate

with 42 Wärtsilä 50SG engines run-

ning on natural gas.

The Wärtsilä equipment is sched-

uled for delivery in 2028, and the

plant is expected to become fully op-

erational in late 2029. This is Wärt-

sil’s fth data centre related order in

the U and its rst in Teas. lto-

gether, Wärtsilä has thus far sold

over 2.4 GW of power capacity for

US data centres.

AtkinsRéalis has announced that it has

signed a Strategic Alliance Agreement

with First American Nuclear (FNCO)

to be the engineering, procurement,

and construction management

(EPCM) provider for EAGL-1 SMR

projects in North America. The agree-

ment contemplates services worth up

to 20 million over the rst ve years.

Under the rst task orders, tkins

Réalis will prepare procedures and

policies required to do design work,

such as a quality programme and

engineering procedures. It will also

undertake the conceptual design for

the balance of plant and review the

design of the nuclear steam supply

system.

EAGL-1 is the only US nuclear re-

actor design cooled by lead-bismuth,

a liquid metal alloy that has been

used in successful nuclear systems

abroad for decades. The unique

properties of lead-bismuth enable a

simpler, more compact reactor de-

sign with fewer components and re-

duced complexity.

Electroguayas, Ecuador’s state power

generator, has awarded a $20 million

contract to upgrade the 90 MW Santa

Elena II thermal plant to HH Interna-

tional of South Korea. HH Internation-

al will increase the capacity of the

plant to 108 MW.

The plant came online in 2011 and

comprises 53 9H21/32 model en-

gines which use diesel for startup

and then operate on fuel oil.

Electroguayas said that Santa Ele-

na’s expansion will reduce depen-

dence on eastern basin reservoirs and

electricity imports during droughts

and El Niño events as well as

strengthen grid stability and voltage

quality, while fast-start internal com-

bustion engines will help meet peak

demand and offset sudden supply

disruptions.

Wärtsilä has signed two equipment

supply contracts with Origem Energia

to develop new balancing power proj-

ects in Brazil. The contracts are for the

supply of two batches of 18 Wärtsilä

34SG balancing engines.

The projects are the Pilar and Pilar

Nova power projects, scheduled to

start operations in October 2028, and

the Manguaba I-V projects, sched-

uled to start operations in August 2.

South Korea’s Hanwha Power has

signed an MOU with Canadian infra-

structure company Pembina Pipeline

to collaborate on green power gener-

ation projects.

Under the terms of the agreement,

Hanwha Power will explore apply-

ing waste heat recovery power gen-

eration systems to Pembina’s pipe-

line compressor stations and gas

infrastructure facilities. Hanwha

Power’s waste heat recovery power

generation system is a next-genera-

tion technology that uses carbon di-

oxide in a supercritical state.

Indonesian state utility PLN has

awarded a 45 MW hydropower project

contract valued at $116 million to

Kencana Energi Lestari (KEEN). The

hydropower plant will be developed

in Pakkat district, Humbang Hasun-

dutan Regency, North Sumatra.

Giat Widjaja, Finance Director of

KEEN, said: “The Pakkat 2 hydro-

power plant is estimated to require

an investment of around $116 mil-

lion, with a construction target of ap-

proximately four years. We are cur-

rently awaiting the signing process

for the Power Purchase Agreement

with PLN before entering the con-

struction phase.”

Indonesia has been accelerating re-

newable-energy development as part

of its broader strategy to reduce de-

pendence on fossil fuels and meet

long-term climate commitments.

DeepOcean has secured a contract for

the installation and support of in-

ter-array cables at the TPC offshore

wind farm phase 2 (TPC-II) offshore

Taiwan. The scope of the contract

covers installation of inter-array ca-

bles, as well as engineering and proj-

ect management services.

The 295 MW project, located 6.5-

20 km off Lukang in Changhua

County, will feature 31 Vestas 9.5

MW turbines installed on jacket

foundations. The turbines will be

connected via three 66 kV inter-ar-

ray cable loops to an offshore sub-

station, with power exported to shore

through three export cables.

The offshore work will be carried

out with Dong Fang Offshore using

the chartered subsea vessel Orient

Adventurer. The work will com-

mence immediately and be complet-

ed during 2026.

South Korea’s Ministry of Climate,

Energy, and Environment has an-

nounced plans to build ten GW-scale

solar power complexes in and near the

greater Seoul area as part of a push to

expand renewable energy capacity and

lower electricity generation costs. This

is part of the ministry’s plan to achieve

100 GW of renewable energy capacity

by 2030.

The government said it will identi-

fy ten agship solar power projects

by 2030, including sites in the Si-

hwa and Hwaong districts. Other

potential locations include Pyeong-

taek Port and Lake Pyeongtaek, for-

mer coal red power plant sites in

the Chungcheong region, and border

areas spanning northern Gyeonggi

Province and Gangwon Province.

Each project will have capacities

ranging from 1 GW to 1.4 GW.

The Asian Development Bank (ADB)

has signed a 6 million nancing

package with ACWA to develop a 300

MW wind power plant in Uzbekistan’s

Bukhara region.

The new facility, Bash 2, extends

the Bash ind ower roject co--

nanced in 2023. Bash 2 will feature

39 turbines, each up to 8 MW, a

35/500 kV substation, and transmis-

sion lines connecting to the national

grid.

The nancing includes 0 million

from ADB’s ordinary capital resourc-

es, $41 million from commercial

lenders with ADB as the lead arrang-

er, as $25 million from the Leading

Asia’s Private Infrastructure Fund 2

(LEAP 2).

RenewRome, a special purpose vehi-

cle owned by Kanadevia Inova, Acea,

Suez, Vianini Lavori and RMB, has

been selected to build and operate a

new waste-to-energy (WtE) plant for

the Municipality of Rome. Kanadevia

Inova will act as the EPC contractor

and will be responsible for plant main-

tenance for 30 years.

The new WtE facility is located in

Santa Palomba, 25 km southwest of

Rome. The new plant will treat

around 600 000 tonnes of non-recy-

clable waste annually and generate

around 6 . The ue gas treat-

ment (FGT) system consists of a

semi-dry unit, a wet scrubber, and a

selective catalytic reduction system

for nitrogen oxide reduction.

Construction work began last

month, and the rst waste delivery is

scheduled for autumn 2029.

Nordex has won orders from West-

fälisch-Niedersächsische Energie

(WNE) for the supply and installation

of 12 N175/6.X wind turbines. The

turbines will be installed across three

projects in the district of Höxter in

North Rhine-Westphalia. The total ca-

pacity of the orders amounts to 82 MW.

The contracts also include a service

agreement for the turbines for 20 years.

Seven turbines will be deployed at

the Dringenberg project, three tur-

bines at the Gehrden Ost project, and

two turbines at the Gehrden Fölsen

extension project. Construction work

is scheduled to start in mid-2027.

Mott MacDonald is providing lend-

er’s technical and environmental sup-

port to the West Wales Hydrogen

project, a production facility that will

deliver 2000 t of low-carbon hydro-

gen annually.

Developed by MorGen Energy, a

large-scale green hydrogen ecosys-

tems developer, West Wales Hydro-

gen is claimed to be the rst proj-

ect-nanced green hydrogen project

in the UK and Europe.

Located at the former oil renery

site in Milford Haven within the

Celtic Freeport of Wales, the project

will feature a 20 MW electrolyser

system supplied by hefeld-based

ITM Power that will be used to pro-

duce the green hydrogen.

Mott MacDonald provided techni-

cal due diligence on the project’s de-

sign, contracting structure, construc-

tion and operational plans, cost and

schedule assumptions, as well as key

risks.

The company is now advising the

lenders on bankability and ongoing

monitoring requirements.

The Ukraine government has an-

nounced that it will hold a competition

to award 322 of new eible

generation in the most energy-decient

regions. Prime Minister Yulia Svy-

rydenko said that these include the

Kyiv and Cherkasy regions (250 MW),

the Sumy, Kharkiv, and Poltava regions

(872 MW), Dnipropetrovsk (100

MW), and Odesa regions (100 MW).

An incentive mechanism will be

provided for participants. The maxi-

mum term for commissioning new

capacities is 20 months.

GE Vernova has won an order from

Middle Delta Electricity Production

Company (DEC), an afliate of

Egyptian Electricity Holding Compa-

ny (EEHC), for projects at MDEPC’s

Bahna and Nubaria power plants in

Egypt. The scope includes two Ad-

vanced Gas Path (AGP) upgrades for

the two GE Vernova 9F gas turbines at

the Bahna power plant, along with

multi-year services agreements for

Bahna and Nubaria with terms of 15

and eight years, respectively.

The upgrades are expected to in-

crease plant output while improving

efciency by about 2 per cent.

Genesis Energy and Saft, a subsidiary

of TotalEnergies, have signed a con-

tract for a 200 MWh extension for the

Huntly battery energy storage system

(BESS). The expansion builds on the

original 100 MW / 200 MWh BESS at

Huntly Power Station on New Zea-

land’s North Island.

With this expansion, Huntly is set

to become one of the largest BESS

sites in the country, reaching a poten-

tial output of 400 MWh, co-located

with a .2 gas and coal red

power station.

Eurus Energy Holding’s Aeolus SAS

(Aeolus) has completed two 50 MW

solar power plants in Tunisia, repre

-

senting Eurus’s rst renewable energy

projects in Tunisia.

The 50 MW solar power plants are

located in Sidi Bouzid Governorate

and Tozeur Governorate and will

supply electricity to approximately

120 000 households in Tunisia.

Operations will be carried out by

operating companies jointly owned

by Aeolus (49 per cent stake) and

Scatec ASA, a Norwegian renewable

energy solutions provider (51 per

cent stake).

Americas

Asia-Pacic

Vestas wins 186 MW

Québec turbine order

AtkinsRéalis wins SMR

EPCM contract

PLN awards $116 million

hydropower contract

DeepOcean wins Taiwan

offshore wind contract

South Korea to build ten

large-scale solar complexes

ADB and ACWA support

Uzbekistan wind power

Waste-to-energy plant to

be built in Rome

Nordex wins 82 MW

German turbine orders

Support for West Wales

Hydrogen project

Ukraine seeks 1.3 GW of

eile eneration

GE Vernova wins upgrade

contracts in Egypt

Next phase of New

Zealand’s Huntly BESS

Aeolus supplies solar

plants to Tunisia

Wärtsilä wins Brazil grid

balancing contracts

Off-grid energy for data

centre in Texas

International

Europe

10

THE ENERGY INDUSTRY TIMES - JUNE 2026

Tenders, Bids & Contracts

Hanwha Power MOU for

Canada green energy

HH International to

upgrade Santa Elena II

Sponsored Editorial

THE ENERGY INDUSTRY TIMES - JUNE 2026

12

D

ata centre construction has always been a

balancing act between speed, scale and resil-

ience. That balance is being tested as never

before. AI workloads are pushing power densities

into territory the industry was not initially prepared

to handle, and operators are being asked to deliver

capacity at a pace that traditional build models strug-

gle to support. The constraint is no longer just land

or chips. It is power, and more specically, the abil-

ity to get power into the building, congured cor-

rectly, and operational on schedule.

This is where the modular electrical switchroom

has quietly become one of the most important

components in the data centre stack. As of recently,

AV K h a v e p o s i t i o n e d t h e m s e l v e s a s a n e x p e r t p r o -

vider of this technology, completing their full

power chain offering.

A gap in the power chain

For all the talk of end-to-end energy partners, the

reality has been that data centre operators have

rarely been able to source their full power infra-

structure from a single provider. Generators have

come from one supplier, switchgear from another,

UPS from a third, and the integration risk has sat

squarely on the operator or main contractor. Mod-

ular electrical switchrooms, the containerised units

that house the critical electrical infrastructure re-

sponsible for safely distributing power throughout

the facility, have typically been a separate procure-

ment exercise altogether.

AV K h a s s p e n t m o r e t h a n 3 6 y e a r s b u i l d i n g e x p e r -

tise in uninterruptible power supplies, standby

power, prime power and control systems. The

component that now completes the picture, the

modular switchroom, was the missing piece. With

the launch of AVK PowerPods, that gap has closed.

PowerPods are fully integrated, pre-engineered,

transportable units that consolidate transformers,

switchgear, UPS, batteries, circuit breakers, cooling

integration, control panels, re suppression, and

distribution boards into a single containerised

solution. Each unit arrives ready to connect and

deploy. With this addition, AVK now provides the

entire power chain for a data centre, covering every

part of the energy lifecycle from generation through

distribution to ongoing maintenance.

AI as the forcing function

The timing of this launch is no accident. Hyperscale

operators and AI infrastructure providers are placing

demands on power delivery that did not exist even

three years ago. Training clusters require contiguous

blocks of power measured in tens or hundreds of

megawatts. Inference workloads need facilities op-

erational quickly enough to keep pace with model

deployment cycles. And the projected growth in AI

compute means that capacity planning is now a con-

tinuous activity rather than a periodic one.

Traditional build models are struggling to keep up.

Stick-built electrical rooms, constructed on site

alongside the rest of the facility, are exposed to

weather, labour availability, supply chain disruption

and the sequential dependencies of site programmes.

Lead times for individual components such as

transformers and switchgear have stretched in re-

cent years, and operators have absorbed both the

cost and the schedule risk.

The modular approach reorders this equation. By

moving construction off-site into a controlled facto-

ry environment, integration testing can be complet-

ed in advance, quality is more consistent, and the

unit arrives at the data centre as a tested system

rather than a collection of parts waiting to be assem-

bled. Construction time on site is reduced, and the

operator gains condence that the euipment has

been validated as an integrated whole.

Built for scale at Haydock

AV K h a s i n v e s t e d i n a 1 4 0 0 0 0 f t

2

facility in Haydock,

northwest England, designed specically to support

the volume that hyperscale and AI infrastructure

projects require. The facility has the capacity to house

22 to 25 PowerPods at any one time, depending on

size, with most units up to 18 m in length and 4.2 m

wide. Multiple access routes allow for fast delivery

to project sites across the UK and into Europe.

The scale of the facility matters because it reects

the scale of the underlying demand. PowerPods are

not a bespoke engineering project repeated occa-

sionally. They are a productionised offering de-

signed for mass deployment, and the factory has

been built around that operational reality. At the

same time, the facility supports full customisation

within each unit, so operators retain the ability to

specify the technology conguration that suits their

requirements.

Technology agnostic by design

One of the structural problems with traditional pow-

er infrastructure procurement is that operators often

end up locked into a single manufacturer’s ecosys-

tem. The choice of UPS dictates the switchgear, the

switchgear dictates the controls, and the architecture

becomes rigid before the facility is even built.

AV K ’ s a p p r o a c h i s d e l i b e r a t e l y d i f f e r e n t . P o w e r -

Pods are designed to be technology-agnostic,

meaning the operator chooses the best component

for each function rather than accepting a bundled

solution. AVK acts as an energy partner, consulting

on the optimal conguration for the project at hand

and sourcing equipment accordingly. The result is

genuine eibility, better lead times due to a broad-

er supply base, and an outcome tailored to the facil-

ity’s specic operational prole.

This matters more in the AI context than in con-

ventional cloud workloads. AI infrastructure has

different thermal proles, different load patterns,

and different redundancy requirements, and the

right technology stack for one operator will not be

the right stack for another. The supplier agnostic

model accommodates that variation in a way that

single-vendor solutions cannot.

A complete proposition

The strategic shift represented by PowerPods is that

AV K i s n o w i n t h e b u s i n e s s o f d e l i v e r i n g h o l i s t i c

and complete power solutions. Generators, UPS,

switchrooms, controls and service all come from the

same partner, which means a single point of account-

ability across the power chain and a single design

philosophy guiding the integration.

Ben Pritchard, CEO at AVK, sees this as the cul-

mination of a long-term direction of travel. “The

launch of AVK PowerPods reinforces our position

as one of the few businesses capable of designing,

delivering and supporting the entire data centre

power ecosystem, at scale, with true eibility and

with the engineering depth that critical infrastruc-

ture demands. PowerPods complete our proposition

to the market. With our ready-to-deploy model, we

are perfectly positioned to support the next wave of

hyperscale data centres and AI infrastructure.”

What this means for the industry

For data centre operators planning their next wave

of capacity, a credible single-source provider for the

full power chain changes the procurement conver-

sation. Integration risk moves to the supplier, sched-

ule certainty improves, and the operator can focus

on the workload-facing decisions that actually dif-

ferentiate their service. The cost of complexity in

multi-vendor power procurement has always been

hidden in programme overruns and commissioning

delays, and removing it has tangible value.

The wider industry implication is that modular,

factory-built power infrastructure is becoming a

necessity rather than a nice-to-have for projects

above a certain scale.

AI has accelerated this transition because the al-

ternative, slower stick-built construction, is no lon-

ger viable at the pace operators need. PowerPods

are AVK’s answer to that shift, grounded in 36 years

of critical power expertise and now positioned at the

centre of how hyperscale facilities will be powered

for the foreseeable future.

AVK has spent more than 36 years building expertise in uninterruptible power supplies,

standby power, prime power and control systems. With the addition of PowerPods, it now

provides the entire power chain for a data centre, covering every part of the energy lifecycle

from generation through distribution to ongoing maintenance.

AVK’s CEO, Ben Pritchard:

PowerPods complete our

proposition to the market

Solving the power bottleneck

holding back AI data centres

I

t was not long after the start of

Russia’s war against Ukraine

that gas and subsequently elec-

tricity prices, began to spiral across

much of the EU. The crisis brought

the realisation that in order to meet

its decarbonisation goals, while en-

suring energy security, Europe must

double-down on efforts to deploy

home-grown renewables such as

offshore wind. The war in Iran pro-

vided another stark reminder as to

why this is paramount.

At the North Sea Summit in Ham-

burg in January this year, European

leaders committed to an accelerated

and more consistent expansion of

offshore wind. And in April at the

WindEurope Annual event in Ma-

drid, just three months after the

Hamburg summit, the industry took

stock of the current situation and

what needs to be done.

In a statement, WindEurope said:

“Europe needs to move from crisis

to condence The war in Iran re-

minded Europe, again, that it needs

to replace imported fossil fuels with

homegrown, secure electricity. Off-

shore wind delivers the energy Eu-

rope needs. It is homegrown, scal-

able and cost-effective. Offshore

wind helps lower electricity costs

for households and businesses. And

it shields Europe from geopolitics

and fuel price swings.”

The North Sea Summit 2026 saw

the governments of Belgium, Den-

mark, France, Germany, Ireland,

Luxembourg, the Netherlands, Nor-

way and the United Kingdom, to-

gether with wind industry players,

and Transmission System Operators

(TSOs) of the electricity and hydro-

gen networks agree the ‘Joint Off-

shore Wind Investment Pact’ for the

North Seas.

All signatories of the Hamburg

Declaration committed to “working

together towards a shared ambition:

to scale offshore wind energy to the

levels required for Europe’s decar-

bonisation, to enable hydrogen as a

complementary energy carrier to

offshore renewable electricity

(where cost-efcient), to ensure af-

fordable and secure energy for citi-

zens and businesses, and to

strengthen Europe’s industrial base

and technological leadership”.

The Hamburg Declaration provid-

ed the political signal Europe’s off-

shore wind supply chain needed.

Governments agreed to contribute to

the build-out of 15 GW of offshore

wind annually from 2031-2040.

CfDs offer visibility on future rev-

enues and help de-risk new wind

energy investments. The volume

commitments offer visibility for

manufacturers and supply chain to

invest in factories, ports and

services.

WindEurope also highlighted the

huge role that industry has to play.

“As its contribution to the Hamburg

Declaration, the European wind in-

dustry committed to cut the costs of

offshore wind by 30 per cent by

2040, compared 2025 levels. This

will come through lower nancing

costs, de-risked projects and faster

industrialisation,” said Tinne van

der Straeten, WindEurope CEO.

“The industry is already delivering.

We are investing in projects, manu-

facturing capacity and skills. And

stepping up on security.”

Yet delivering on the goals re-

mains a tall order. One major obsta-

cle is grid buildout. Commenting on

the threat, Alfredo Parres, Hitachi

Energy’s Global Head of Renew-

ables, and Wind Europe Executive

Committee member, said: “It’s real;

we already see it. If you look

around the world, hundreds of giga-

watts are waiting in connection

queues. But the good thing about

the situation is that the problem is

too big to be ignored. It’s very

much a central topic and we don’t

need to convince people that the

challenge needs to be addressed.

[But] maybe we need to push a bit

further to say grids are not just im-

portant – they are a strategic asset,

especially when you think about the

security agenda.”

Pointing out the impacts of the

grid situation, Parres noted that ca-

pacity cannot be connected on ei-

ther the generation or demand side.

“Industries cannot connect to get

more power, and operating units are

curtailed because the grids are satu-

rated or the energy they put on the

market cause negative prices,” he

said.

Spain, for example, which was a

success story in terms of renew-

ables deployment, has been at a

standstill for a while, resulting in

negative prices. In the UK, where

large amounts of future offshore

wind capacity has been locked in

through its auction process, many

projects have no connection dates

before 2032/33.

Still, despite the challenges, Par-

res offered evidence of progress.

Since the Hamburg declaration, off-

shore wind generation targets have

been conrmed, with an emphasis

on hybrid projects that combine

wind power projects and intercon-

nection projects.

“The Hamburg declaration takes

the Copenhagen call to action from

WindEurope’s annual event last

year further in terms of the level of

detail of what needs to be done. It

highlights the need to have an inte-

grated system to deliver electrica-

tion, and nancing,” said arres.

“The UK’s AR7 [Auction round 7],

with an increased budget and secur-

ing 7 GW of new capacity, is a good

example of what can be done. And

indicates that AR8 could be just as

good as AR7.”

In countries like the Netherlands,

Denmark and Germany, where there

were failed auctions, governments

revised auction models to further

de-risk projects by moving to CfDs.

“For me, this is absolutely moving

in the right direction. It is the best

tool right now to help lock-in more

generation and more projects,” said

Parres.

Looking at the rest of the agenda,

he says there is a need to continue

working on the infrastructure – how

to put the offshore network in place.

“Cost allocation for projects that go

across countries is very tricky; very

sensitive and we need to it,” he

noted. “We need to talk about the

relationship between the UK and

EU so that we can be closer again

on the energy agenda.”

Continuing to build up the supply

chain and ensuring the huge genera-

tion plans turn into contracts must

be a priority. To this end, suppliers

like Hitachi Energy have been en-

tering framework or programme

agreements so that several projects

can be considered together in order

to create supply chain efciencies

and thereby reduce costs. This will

ultimately contribute to affordabili-

ty for consumers.

In its current investment pro-

gramme, Hitachi Energy has allo-

cated €9 billion to 2027 to ramp up

the manufacturing and resources

needed to meet the demand.

Parres noted: “This investment

comes with 15 000 people who will

be hired and trained to develop a

career in a satisfying, vibrant work

environment where they can grow.”

Notably, money and resources will

be invested in segments such as

transformers, circuit breakers and

high voltage direct current (HVDC).

This long term, frame agreement

approach was taken to not only

meet forecasted demand, but also to

address how project developers are

changing their market approach.

“When we saw how TenneT, for

example, came to the market with a

2 GW programme for HVDC –

bringing 11 connections to the mar-

ket in one go, and splitting those

volumes between three main suppli-

ers – that gave us visibility. It gave

us certainty on future needs and

provided the motivation for us to

invest big-time,” said Parres. “Simi-

larly, a programme agreement with

E.On on distribution transformers

over several years gave us clarity on

what was coming.”

While this will help deliver proj-

ects faster and cut costs, achieving

the 30 per reduction in LCOE,

which equipment manufacturers

agreed under the Hamburg declara-

tion, is multi-faceted.

Unit capacity factor, said Parres,

is the rst item the industry must

address. In the same way that a 15

turbine is more cost-efcient

than a 10 MW machine, a 2 GW

DC link is more efcient than a

1 GW link.

“Everything that brings more

power, reduces the cost of a kilo-

watt-hour; so size matters,” ex-

plained Parres. “Technology helps

us to increase power density.”

The second area is efciency, said

Parres. “If you can optimise how

the whole system is designed from

an electrical standpoint, you can re-

duce losses, which contributes to a

lower LCOE. Here, HVDC reduces

losses big-time.”

Standardisation, through things

like frame agreements, is the third

part of lowering LCOE said Parres,

citing the agreement signed in Ma-

drid with Danish renewables devel-

oper, Ørsted. Collaborating more

closely with project developers,

through such agreements allows

more optimised designs to be

brought to market.

But LCOE is not just about cost; it

is also about revenue. “With LCOE

we can also address revenue – get-

ting more through the lines, having

less curtailment; having more ener-

gy in the system,” said Parres. “The

point is, there is no single magic

bullet. It’s not about squeezing the

supply chain even more – we’re not

in favour of a race to the bottom –

reducing margins and putting the

industry in losses. We saw what

happened with wind turbine manu-

facturers. It’s better to collaborate;

increase efciencies so everyone

can make reasonable margins.”

He concluded: “Going forward

from Madrid, we need to think and

talk holistically. Move away from

point-to-point solutions to system

solutions, where all the stakeholders

develop, in a harmonious way, the

generation, grid and the offtake.

And combine it with longer term

planning This is where we need

to go and it’s where we are going.

That’s the mission I have left Ma-

drid with that’s the ag I’m ying.”

The energy crises, triggered by wars in Ukraine and Iran, have spurred Europe to accelerate its offshore wind

abition but the challenges are signicant ollowing the indEurope event in adrid Junior Isles caught up with

itachi Energys lfredo arres to discuss those challenges and what real progress is being ade

Offshore wind: from

Offshore wind: from

Hamburg to Madrid

Hamburg to Madrid

THE ENERGY INDUSTRY TIMES - JUNE 2026

13

Energy Outlook

Parres: “We need to think and talk

holistically… That’s the mission I

have left Madrid with”

Photo by pexels.com

of $15.5 billion. In addition, Vietnam

issued a Revised Power Development

Plan 8 (PDP8) and amended its Elec-

tricity Law.

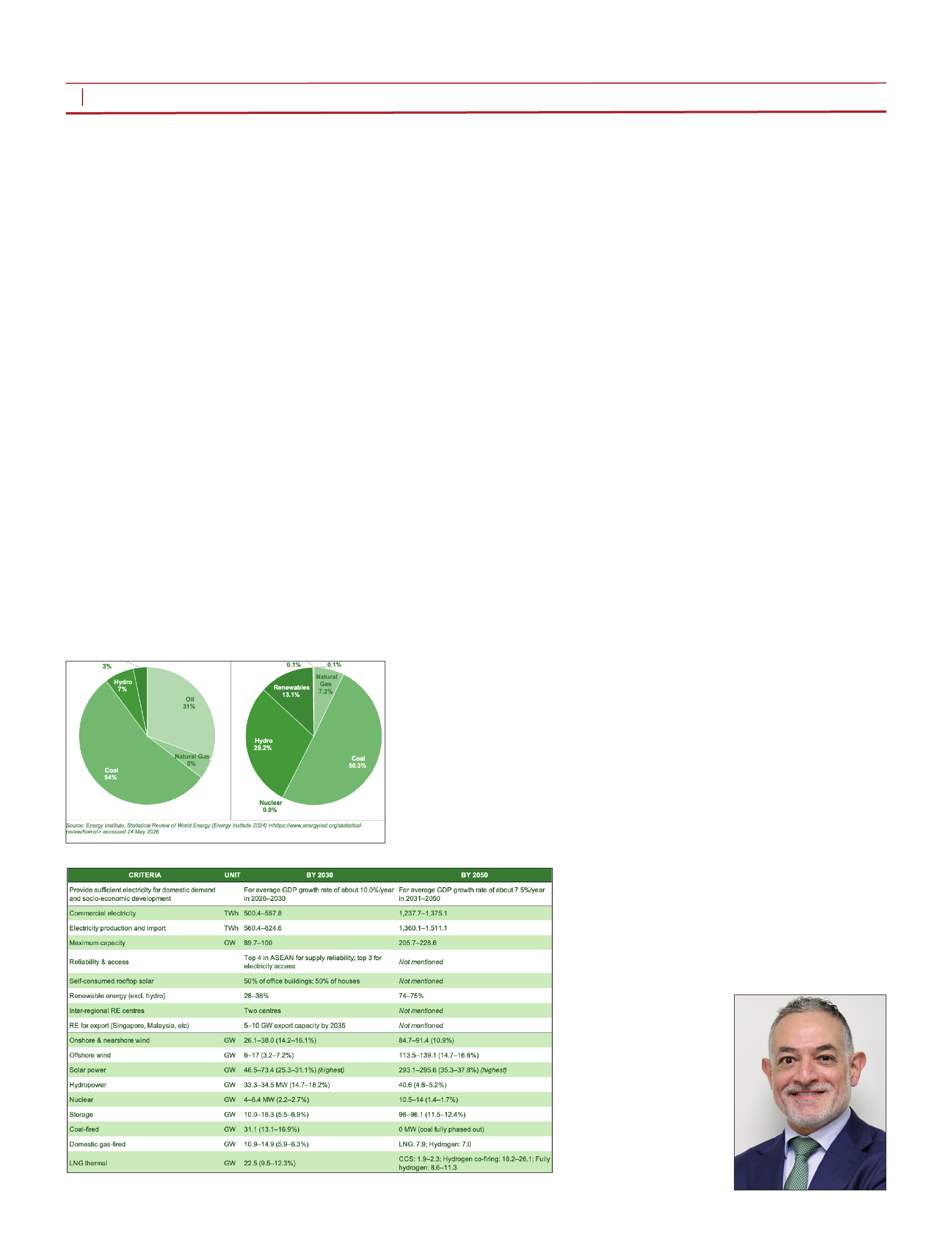

Energy mix

Vietnam’s primary energy supply is

heavily dominated by fossil fuels. Coal

accounted for more than half of the

total mix and oil contributed a further

31 per cent in 2024. Natural gas plays

a relatively modest role at just over 7

per cent, while hydro represents only

7 per cent of supply. Non-hydro re-

newables barely register at 3 per cent,

and other sources are negligible. The

electricity generation prole is simi-

larly shaped by coal, which provided

just over half of all power produced,

also in 2024. Hydropower was the

second largest contributor at around

2 per cent, reecting the country’s

longstanding reliance on its river sys-

tems. Renewables made up a more

visible share of generation at 13.1 per

cent, though still far below the levels

required for a rapid transition. Natural

gas contributed 7.2 per cent, and there

was no contribution from oil and nu-

clear (see pie chart).

The amended PDP8, released in

April 2025, outlines a steep expansion

of electricity demand and system ca-

pacity through 2030 and 2050 (see

chart). Commercial electricity con-

sumption is projected to more than

double by mid-century, while total

capacity rises to over 205 GW by

2050 from roughly 90-100 GW in

2030. The plan accelerates a structur-

al shift towards renewables, with

non-hydro sources reaching up to

three-quarters of the mix by 2050,

alongside major growth in offshore

wind, solar, and storage. Coal is fully

phased out, while gas transitions

progressively towards hydrogen and

CCS-enabled technologies.

Transmission and distribution con-

straints and curtailment are, unsur-

prisingly, a key challenge to the path

to net zero for a nation experiencing

V

ietnam’s energy transition is

reaching a critical turning

point. Investors face a complex

mix of rapid growth and systemic chal-

lenges, as the country accelerates to-

ward 2050 net zero goals. Beyond the

potential for renewable expansion,

successful ventures require navigating

infrastructure bottlenecks, regulatory

shifts, and structural market hurdles.

Decarbonisation commitments

ietnam has taken signicant steps in

recent years on its path to decarboni-

sation, despite facing a great many

hurdles. The country updated its cli-

mate commitments under the Paris

Agreement through the publication of

its Nationally Determined Contribu-

tion (NDC) in October 2022. It raised

its targets to cut greenhouse gas emis-

sions. On its own, without outside

help, it pledged to reduce emissions

by 15.8 per cent below projected levels

by 2030, up from 9 per cent previous-

ly. ith international nancial sup-

port, that gure rises to 3. per cent,

compared to 27 per cent before.

The updated NDC is more ambi-

tious on paper, but independent as-

sessments suggest it falls short of

genuine progress, according to the

Climate Action Tracker, an indepen-

dent scientic assessment of national

climate action, as of late 2025. The

targets remain consistent with around