www.teitimes.com

April 2019 • Volume 12 • No 2 • Published monthly • ISSN 1757-7365

THE ENERGY INDUSTRY TIMES is published by Man in Black Media • www.mibmedia.com • Editor-in-Chief: Junior Isles • For all enquiries email: enquiries@teitimes.com

Special Technology

supplement

Is AI the saviour?

A megaproject is under way that

is aimed at turning Bolivia into a

regional energy hub.

Unlocking big data through articial

intelligence could be key to the survival

of energy companies.

Page 13

News In Brief

Green hydrogen becoming

affordable alternative

The outlook for hydrogen as

an energy carrier is looking

increasingly promising, according to

recent research.

Page 2

NY reveals storage

incentives

New York state is keeping its energy

storage targets with a proposed

package of incentives

Page 4

Japan releases results of

V2G experiment

Mitsubishi Motors has released

results of a ‘Vehicle-to-Grid’ (V2G)

experiment undertaken by seven

Japanese companies.

Page 6

Finland moves to phase out

coal

Finland has approved proposals

to stop using coal for energy

production in 2029.

Page 7

South Africa faces power

shortages once more

South Africa’s economy is suffering

in the country’s latest round of load

shedding events.

Page 8

Shell increases electric

utility activity

Shell has accelerated its move into

the utility sector with the acquisition

of Limejump, a UK-based demand

side aggregator.

Page 9

Energy Outlook: A battery-

powered renewable future

Battery storage will reduce

costs, improve energy security

and increase renewables in the

generation mix. The question is how

to increase global deployment.

Page 14

Technology: Hydrogen and

electricity from plastic

A new process for the conversion

of waste – typically unrecyclable

plastic and used tyres – into

hydrogen and electricity has

been assessed and is now in the

commercialisation phase.

Page 15

Advertise

advertising@teitimes.com

Subscribe

subscriptions@teitimes.com

or call +44 208 523 2573

In a drive to accelerate clean deployment efforts in developing countries, the World Bank

Group and Global Wind Energy Council are working together to fast-track a growing pipeline

of offshore wind projects. Junior Isles

Carbon emissions reaches all-time high despite

renewables growth

THE ENERGY INDUSTRY

TIMES

Final Word

The UK’s green gas plan

is a bold one, says

Junior Isles.

Page 16

The World Bank Group (WBG) is

looking to accelerate the adoption of

offshore wind energy in developing

countries.

Under the new programme, the

World Bank and sister organisation

International Finance Corporation

(IFC) will help emerging markets as-

sess their offshore wind potential and

provide technical assistance to devel-

op a growing pipeline of projects that

are ready for investment by renewable

energy developers.

This work will be carried out in co-

operation with the Global Wind En-

ergy Council (GWEC) and its recently

formed Offshore Wind Task Force,

which brings together leading off-

shore wind developers, equipment

manufacturers and service providers.

Led by the World Bank’s Energy

Sector Management Assistance Pro-

gram (ESMAP), the $5 million pro-

gramme is being initiated thanks to a

£20 million ($26.4 million) grant to

ESMAP from the United Kingdom

government to help low- and middle-

income countries implement environ-

mentally sustainable energy solutions.

The initiative presents an important

opportunity for countries with strong

offshore wind resources, including

Brazil, Indonesia, India, the Philip-

pines, South Africa, Sri Lanka and

Vietnam. Vietnam’s technical poten-

tial for xed and oating offshore

wind is 309 GW, while South Africa

and Brazil have 356 GW and 526 GW

in total technical offshore wind poten-

tial, respectively.

The programme will bring together

developing country governments,

commercial developers, development

partners and wind energy experts to

raise awareness around offshore wind

opportunities in emerging markets

and lay the groundwork for a pipeline

of new projects that could be support-

ed by World Bank or IFC nancing.

The World Bank and IFC will work

with public and private sector partners

to undertake technical studies and de-

velop national strategies to facilitate

the adoption of this increasingly cost-

competitive technology.

According to the World Bank, off-

shore wind has grown nearly ve-

fold since 2011, with 23 GW installed

at the end of 2018 and a large volume

of planned projects in Europe, China

and the United States. Offshore wind

now represents about $26 billion in

annual investments or 8 per cent of

new global investments in clean en-

ergy and this proportion is set to in-

crease dramatically, with about $500

billion expected to be invested in

offshore wind projects by 2030.

“Offshore wind has already made

signicant strides in markets such as

Europe and China, but its true

potential reaches far beyond these es-

tablished areas,” Ben Backwell, CEO

at GWEC, said.

Riccardo Puliti, Senior Director and

Head of Energy and Extractives at the

World Bank added: “Offshore wind is

a clean, reliable and secure source of

energy with massive potential to

transform the energy mix in countries

that have great wind resources. We

have seen it work in Europe – we can

Continued on Page 2

Rapid growth in wind and solar was

not sufcient to prevent carbon diox-

ide emissions reaching a historic high

in 2018, according to an International

Energy Agency (IEA) report.

In its latest assessment of global en-

ergy consumption and energy-related

CO

2

emissions for 2018, the IEA

found that energy demand worldwide

grew by 2.3 per cent last year, the fast-

est pace this decade, with fossil fuels

meeting nearly 70 per cent of the

growth for the second year running.

According to the ‘Global Energy &

CO

2

Status Report’, the rapid growth

in energy demand was driven by a ro-

bust global economy and stronger

heating and cooling needs in some

regions. Natural gas emerged as the

fuel of choice, posting the biggest

gains and accounting for 45 per cent

of the rise in energy consumption.

Gas demand growth was especially

strong in the United States and China.

Solar and wind generation grew at

double-digit pace, with solar alone

increasing by 31 per cent. This, how-

ever, was not fast enough to meet

higher electricity demand around the

world, which also drove up coal use.

As a result, global energy-related

CO

2

emissions rose by 1.7 per cent to

33 Gt in 2018. Coal use in power gen-

eration alone surpassed 10 Gt, ac-

counting for a third of the total in-

crease. Most of that came from a

young eet of coal power plants in

developing Asia. The majority of coal

red generation capacity today is

found in Asia, with 12-year-old plants

on average, decades short of average

lifetimes of around 50 years.

The report says electricity contin-

ues to position itself as the “fuel” of

the future, with global electricity de-

mand growing by 4 per cent in 2018

to more than 23 000 TWh. This rapid

growth is pushing electricity towards

a 20 per cent share in total nal con-

sumption of energy. Increasing pow-

er generation was responsible for

half of the growth in primary energy

demand.

Renewables were a major contribu-

tor to this power generation expan-

sion, accounting for nearly half of

electricity demand growth. China re-

mains the leader in renewables, both

for wind and solar, followed by Eu-

rope and the US.

Energy intensity improved by 1.3

per cent last year, just half the rate of

the period between 2014-2016. This

third consecutive year of slowdown

was the result of weaker energy ef-

ciency policy implementation and

strong demand growth in more energy

intensive economies.

Commenting on the ndings, Dr

Fatih Birol, the IEA’s Executive Di-

rector, said: “Despite major growth

in renewables, global emissions are

still rising, demonstrating once again

that more urgent action is needed on

all fronts – developing all clean en-

ergy solutions, curbing emissions,

improving efciency, and spurring

investments and innovation, includ-

ing in carbon capture, utilisation and

storage.”

World Bank

Group pushes

offshore wind in

emerging markets

THE ENERGY INDUSTRY TIMES - APRIL 2019

3

POWER SUMMIT 2019

NEW LEADERSHIP

20-21 May, Florence

New concepts, new business models,

new perspectives. Join to discuss new

leadership in the electricity industry with

top of the class speakers.

Hosted by

EUBCE 2019

27

th

European Biomass

Conference & Exhibition

27 - 30 MAY 2019 | LISBON - PORTUGAL

The largest gathering

of biomass experts

www.eubce.com

#EUBCE

THE ENERGY INDUSTRY TIMES - APRIL 2019

5

Asia News

Syed Ali

Large hydropower plants (HPPs) will

become part of the non-solar Renew-

able Purchase Obligation (RPO) in

India, as the government moves to

support the expansion of hydropower

generation and clean energy in the

country.

In March the Union Cabinet gave the

thumbs-up to a number of measures

that would allow India to take advan-

tage of its signicant hydropower po-

tential, estimated at 145.3 GW. Only

45.4 GW of this has been tapped so far.

One of the measures includes the clas-

sication of large hydro as renewable

energy – until now this was reserved

only for projects of up to 25 MW.

It is not yet clear how the RPO scheme

would change in order to include large

hydropower. Indian consultancy RE-

Connect Energy, said: “This change

will prove complex to implement and

may meet with resistance from many

states. One option available would be

to just incorporate large hydro in the

existing Non-solar RPO. However, this

will put a strong negative pressure on

REC [renewable energy certicate]

prices and future non-solar (primarily

wind) capacity addition.”

Following the decision, state-owned

hydropower producer NHPC (Nation-

al Hydroelectric Power Corporation)

announced plans to raise its installed

power generation capacity by approx-

imately 30 per cent by 2022 to reach a

total of 10 GW. The company plans to

spend Rs38 billion ($544 million) for

the scal year to March 2020 as a rst

step to reach this objective.

News to include large hydro as part

of the non-solar RPO comes as the

country saw a slowdown in growth of

wind capacity additions. At the start

of March, Crisil Research said a shift

to a competitive bidding mechanism

has slowed industry growth due to a

signicant fall in tariffs, triggering a

decline in both bid response and prof-

itability for original equipment manu-

facturers (OEMs).

The company added that the wind

energy sector is likely to see a slow

growth with regard to capacity addi-

tions over the next ve years.

It said in a statement that capacity

additions are expected to rise by 14-16

GW over scal 2019 to 2023, entailing

investments of Rs1100 billion ($16

billion). New capacity will mainly be

driven by central government alloca-

tions with relatively stronger counter

parties like Solar Energy Corporation

of India (SECI) and PTC India (for-

merly known as Power Trading Cor-

poration of India), reducing risk as

compared to direct exposure to state

distribution companies.

State auctioning, on the other hand,

has slowed as several states have

signed power supply agreements

(PSAs) with PTC and SECI to procure

wind power under the schemes auc-

tioned by them, to help full their non-

solar renewable purchase obligations

targets.

Crisil also said that moving to a com-

petitive bidding mechanism sector has

caused a slowdown in additions, as

participants are yet to adjust, with tar-

iffs having fallen to Rs2.4-2.6 per unit,

from Rs4-4.5 per unit under the feed-

in-tariff regime.

India has been taking signicant ac-

tion to boost its clean energy and re-

cently signed a major deal with the US

to build six nuclear power plants.

The agreement came after the ninth

round of India-US Strategic Security

Dialogue in March. A statement issued

by the Ministry of External Affairs

(MEA) said: “They committed to

strengthening bilateral security and

civil nuclear cooperation, including the

establishment of six US nuclear power

plants in India.”

The statement seeks to breathe new

life into the civil nuclear cooperation

agreement between the two countries,

which has failed to live up to expecta-

tions since it was signed in 2008.

A law limiting civil liability for

nuclear damages from the plants

passed in 2010 was meant to over-

come a stumbling block for US com-

panies looking to set up nuclear

power plants in India.

However, nancial problems at US

company Westinghouse, which had

agreed in 2016 to build six plants in

Andhra Pradesh, put the plans on hold

when it went into bankruptcy in 2017.

Now owned by Brookeld Asset Man-

agement, Westinghouse has received

the backing of the Trump administra-

tion for the project and US Energy

Secretary Rick Perry promoted it dur-

ing a visit to India last year.

India has ambitious plans to increase

its nuclear electric generation capacity

to meets its growing needs with clean

energy.

Key role for hydro in

India’s clean energy

expansion

n Hydro projects above 25 MW now part of non-solar RPO n US deal signed for six nuclear plants

Bangladesh is planning to raise $2 bil-

lion through issuing bonds to bankroll

investment in the power and energy

sector, according to State Minister for

Power, Energy and Mineral resources,

Nasrul Hamid.

“I am trying to oat an energy pow-

er bond at least for $2 billion,” he said.

“Two things we will get from there:

nance; and branding Bangladesh as

an investment destination. If I become

successful in raising $2 billion, albeit

a small amount given what we need in

the power and energy sector, the whole

world will be eager to invest in the

country.”

The country is already beginning to

prove an attractive destination for

overseas investors. In late February,

Arab Investment Development Au-

thority (AIDA) committed $5 billion

of investment to develop 5 GW of so-

lar power plants in cooperation with

Almaden Emirates Fortune Power

(AEFP) and Bangladesh-based In-

traco Solar Power (ISP).

The solar power project along with

the manufacturing facility, which is to

be completed within the next 6-8 years,

will be powered by a total of 14 million

solar panels, making it the largest solar

power plant investment in Bangladesh.

Commenting on the project, Adil Al

Otaiba, Chairman of AIDA, said:

“The project is likely to reduce pow-

er costs by billions as well as create

jobs for both the power plants and the

proposed solar manufacturing facility

based on an annual 500 MW capacity.

The development will reach its max-

imum capacity by 2030, in line with

the expectations of the government of

Bangladesh.”

Safa Capital Limited (SCL) a com-

pany regulated by Dubai Financial

Services Authority, is the lead nancial

advisor and arranger for the project.

n In mid-March the government

signed ve separate contracts with

Summit Corporation Limited and GE

Consortium for constructing a com-

bined cycle power plant at Megh-

naghat, Narayanganj with a power

generating capacity of 583 MW. Ac-

cording to sources at Power and En-

ergy Ministry, Summit and GE are

scheduled to complete the power

plant by March 2022.

Bangladesh moves

to attract energy

investment

THE ENERGY INDUSTRY TIMES - APRIL 2019

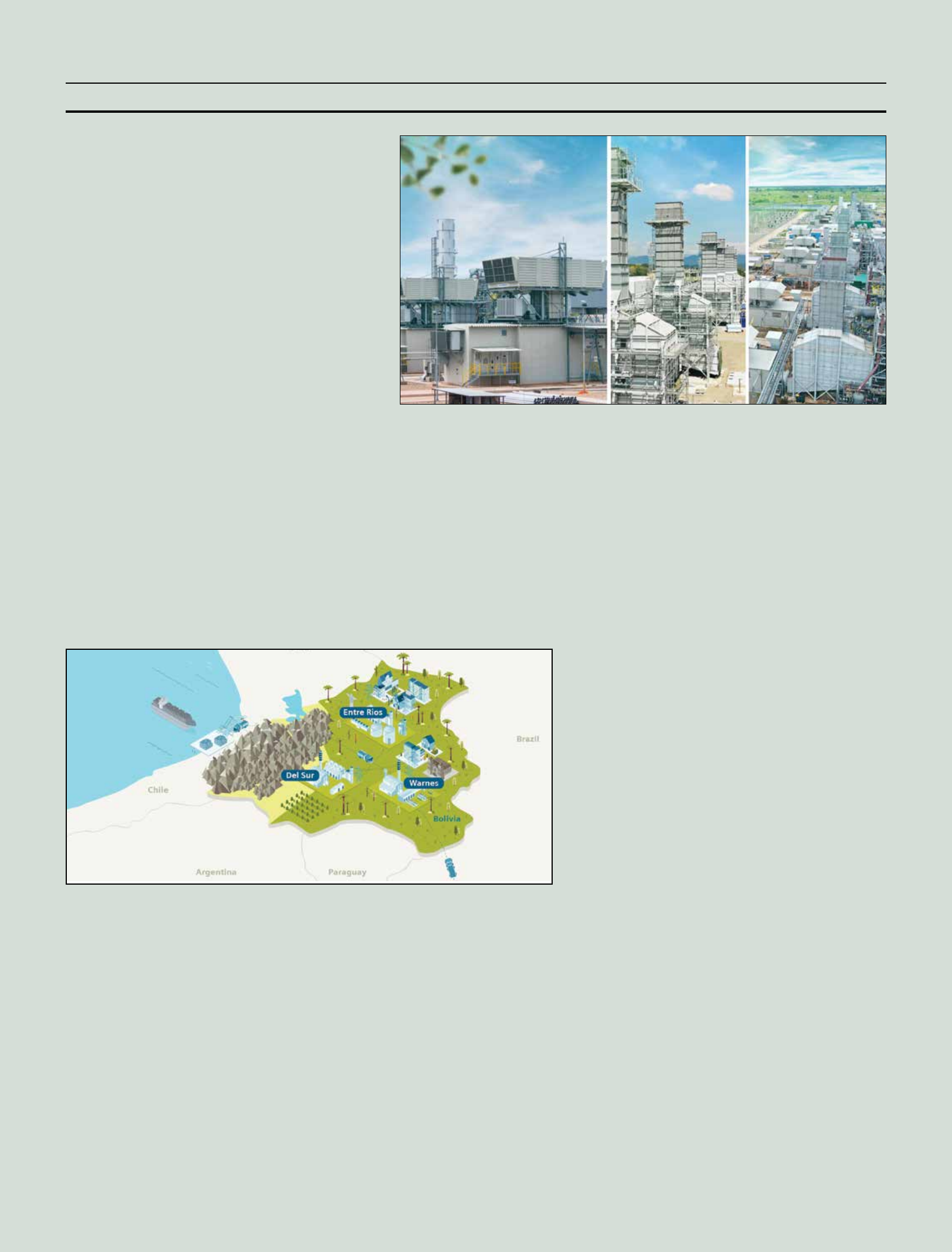

Special Project Supplement

Energising Bolivia

A megaproject is

under way in Bolivia

that is part of a

strategic programme

aimed at turning

the country into a

regional energy hub.

The project, which

sees the conversion

of three separate

simple cycle plants

into combined cycle,

is a showcase in

project logistics

under challenging

conditions.

Junior Isles

what has been a logistically very chal-

lenging project.

In a mega project that will see the

plants converted from open cycle to

combined cycle, Siemens will supply

and commission: four SGT-800 gas

turbines, four SST-400 steam turbines

and eight HRSGs at Termoeléctrica

del Sur; four SGT-800 gas turbines,

four SST-400 steam turbines and

eight HRSGs at Termoeléctrica de

Warnes; and six SGT-800 gas tur-

bines, three SST-400 steam turbines,

and six HRSGs at Termoeléctrica

Entre Ríos.

The main aim of the new contract is

to boost the output of the three plants

and improve efciency. The exten-

sion will see the power output from

Termoeléctrica del Sur increase from

120 MW to about 480 MW; output

from Termoeléctrica de Warnes will

be increased from 200 MW to about

520 MW; and Termoeléctrica Entre

Ríos will see its capacity boosted

from 100 MW to about 480 MW.

Siemens is familiar with the power

plants, having installed the existing

13 gas turbines, which have been

operating at the sites for a number of

years. There are already four existing

SGT-800 turbines at del Sur and ve

at de Warnes; Entre Ríos has four

SGT-700s. The conversion of these

plants to combined cycle, through

the addition of HRSGs and steam

turbines, will increase plant ef-

ciency from round 40 per cent to

50-52 per cent, depending on ambi-

ent conditions.

Commenting on the decision to opt

for Siemens equipment for the proj-

ects, Josef Entfellner, Overall Project

Director, said: “The easiest thing for

the client is to use the same gas tur-

bines they already had for the exten-

sion. It’s easier for them to handle, it’s

easier for spare parts and for mainte-

nance. There is an existing mainte-

nance contract for the gas turbines in

the country, and this has been ex-

tended for the new units.”

The Termoeléctrica del Sur and de

Warnes projects are very similar. In

addition to steam tailing of the exist-

ing units, both will also feature two

completely new combined cycle

blocks, also in a ‘2-on-1’ congura-

tion. Each block comprises two gas

turbines, each with an associated

HRSG that will feed steam to a single

A

s a commodity, energy, espe-

cially gas, is key to Bolivia’s

economic development. With

sizeable gas reserves, the country is an

important energy provider to its neigh-

bours, exporting gas to Brazil and

Argentina. Further, in 2015 Bolivia

had an installed electricity generating

capacity of nearly 2000 MW with gas

accounting for 57 per cent of the an-

nual 9 TWh generation.

Several years ago, in a move to

capitalise on its gas reserves while at

the same time increasing the electri-

cation rate in the country, the govern-

ment took the decision to expand

three of its strategic gas red power

plants. The expansion project would

not only enable the country to ef-

ciently use more of its gas for domes-

tic power production but would also

allow it to export some of that elec-

tricity to its bordering countries and

become an energy hub for the region.

Implementation of that decision

began in 2015 when Bolivia’s Energy

Ministry and Siemens agreed on an

energy collaboration with the goal of

adding roughly 1100 MW to the na-

tional power grid.

Siemens and its consortium partner,

Spanish company TSK, signed a

contract with state-owned electricity

generator Ende Andina S.A.M in

2016 to expand three existing simple

cycle power plants – Termoeléctrica

del Sur, Termoeléctrica de Warnes,

and Termoeléctrica Entre Ríos.

The project is part of a wider vision

for development of the country’s

power sector to reach 100 per cent

electrication by the middle of the

next decade. Known as Vision 2025,

Bolivia is developing projects that

will see generating capacity go from

1924 MW in 2015 to 6000 MW in

2025, of which 3000 MW will be for

export. The plan will see a major

boost for renewables including wind,

solar, biomass, geothermal and hy-

droelectric power generation. But

with gas providing the bulk of genera-

tion, and expected to maintain a sig-

nicant share in the generating mix,

gas red combined cycle technology

is a key part of realising the vision.

Certainly, Bolivia is now undergo-

ing change. It is experiencing a

transformation process in its hydro-

carbon sector, in its industry, road

transport development, and in its

electricity sector. Ende Andina was

initially entrusted with the task of

guaranteeing electricity supply in the

national grid by building its rst gas

red power plant at Entre Ríos.

It was then assigned the task of in-

creasing system reliability by install-

ing additional power through the del

Sur and Warnes projects in the rst

open cycle stage. Today Ende Andina

has the task of changing the genera-

tion technology by moving current

open cycle plants to combined cycle

systems

Ramiro Becerra Flores, Project

lead, Ende Andina, said: “Incorporat-

ing new technology is fundamental

because the gas/energy conversion

process is more efcient and gives the

country the opportunity to nd other

uses for the surplus or residual

amounts of gas that are going to be

produced as a result of mainstreaming

this more efcient new technology.

The scale of the projects, not only

with regard to the electricity industry

but for projects in general in Bolivia,

presents challenges, above all for ex-

ample in the eld of logistics.”

Under the contract, Siemens’ scope

of supply includes the delivery of a

total of 14 industrial gas turbines, 11

steam turbines, 22 heat recovery

steam generators (HRSGs), and other

power plant equipment to Bolivia, in

The expansion project will,

among other things, allow

Bolivia to export electricity to

its bordering countries and

become an energy hub for the

region

turbines, whenever possible.

The rst gas turbine was loaded

onto a ship in Norköping, Sweden.

The ship then travelled to the port of

Hamburg, Germany, where the gas

and steam turbine generators and

other auxiliaries for the gas turbine

were brought on board. The ship then

travelled to Arica, Chile, through the

Panama Canal. In Arica, the parts

were unloaded and trucked to each

project site.

With equipment arriving from sev-

eral countries, different ports of entry

had to be used, as a single port was not

large enough to handle all the cargo.

For the 22 boilers, each consisting of

two modules, a total of 44 boiler

modules were shipped from China to

the ports of Angamos and Arica,

Chile, and then transported on to the

project sites.

It took approximately ve to eight

weeks to ship the gas turbines by sea

from Sweden or Germany to the port

of Arica and then roughly four weeks

to transport them onward to the con-

struction sites.

With limitations on trucks capable

of transporting equipment, it was im-

possible to transport equipment to all

three sites in parallel. Deliveries were

therefore staggered to ship a maxi-

mum of four boilers at one time and

two gas turbines on one vessel.

The main challenge began when

equipment arrived in the country.

Landlocked Bolivia is the highest and

most isolated country in South

America. It has a varied terrain span-

ning the Andes Mountains, the Ataca-

ma Desert and Amazon Basin rainfor-

est. Much of the equipment had to be

navigated across the Andes at a height

of 4680 m.

Many challenges were encountered

at a number of points on the land

routes. Crossing bridges and rivers, as

well as coping with the rainy season,

were some of the key challenges

faced in implementing the project.

The constantly changing and often

extreme weather conditions along the

route (heat, snow, heavy rain, mud-

slides, ooding), presented a special

challenge.

“We had to cross different climatic

zones and the transport on the truck

itself was a huge effort,” said Koerber.

“Normally we try to keep truck trans-

port for heavy-lift equipment as short

as possible. But for this project, in

some instances we had to travel over

1800 km to reach a site with 100

heavy-lift cargoes.”

Transporting the boilers was partic-

ularly challenging. “They are very

large pieces of equipment, weighing

around 170 t. It required several

trucks to pull or push the weight over

the Andes,” said Koerber.

Some journeys involved crossing

50 bridges, with many requiring the

construction of temporary metal sup-

ports. In some cases, new roads had to

be built. “We did a study even before

the project began to make sure it was

all feasible,” said Koerber.

He added: “In South America, you

always need to have communication

with the local authorities. The rst

road may be ne but on the second

there may be a problem; and in Bo-

livia not all the roads are paved. We

needed to be exible to nd a new

road if necessary or change plan to

nd the best solution to get the equip-

ment to site in time.”

Entre Ríos provided a good example

of the adaptability of the logistics

team. Along the route to the plant,

there were two bridges that were too

high to be supported. The team there-

fore took the decision to transport the

six HRSGs from Chile to Bolivia by

aeroplane.

“We had to use the world’s biggest

cargo plane, the Antonov An-225, to

get the heavy equipment past these

bridges and to deliver what we prom-

ised to the customer,” said Koerber.

“We had 12 deliveries; it was a huge

effort.”

The rst gas turbines arrived at del

Sur in August 2017, four months after

leaving Sweden. The rst steam tur-

bine from Brazil also arrived in Au-

gust. There was approximately a

two-month stagger between the three

plants, with Warnes following two

months after del Sur and Entre Ríos,

two months after Warnes.

Erection began as soon as main

equipment began arriving at the sites.

At the peak of construction, there

were more than 1700 people deployed

across the three sites.

A major milestone was reached on

September 18, 2018 with rst re of

the rst two new gas turbines at Ter-

moeléctrica del Sur. Firing of the next

steam turbine. The fth of the existing

gas turbines at de Warnes will remain

in open cycle.

These two plants will also be cooled

differently. Due to its location in the

south of the country, where the condi-

tions are dry, Termoeléctrica del Sur

will use air-cooled condensers. As

Termoeléctrica de Warnes is in an

area where there are small rivers and

wells and rainfall is high, cooling

towers will be employed.

At Entre Ríos, the existing gas tur-

bines will all remain in open cycle.

The new equipment will be used to

build three new 2-on-1 combined cy-

cle blocks. With the availability of

sufcient cooling water, this plant

will also use cooling towers, which

allows slightly higher efciency than

air-cooled condensers.

The decision to keep some of the

gas turbines at the plant in open cycle

allowed each of the combined cycle

blocks to be designed identically. This

not only reduces costs but also means

that the open cycle units can be kept

for use at times of peak demand.

The three plants are geographically

spread in different parts of the coun-

try, and were selected for expansion,

as opposed to building a single new

large facility, for several reasons.

The high voltage grid connections

were already available, as was cool-

ing water, and smaller plants provide

more exibility in terms of power

output and speed of start-up. Further,

the transport of the heavy equipment

that would have been required for a

larger plant would have been almost

impossible.

Each site is also at a fairly low alti-

tude. Bolivia is perhaps ve times

bigger than Germany but only has a

population of around 11 million,

mostly living in two or three major

cities. While it might be expected that

a power plant could be located close

to areas of high load, a couple of those

cities are at a high elevation.

Entfellner noted: “The power plants

are between 200-400 m above sea

level. La Paz, which has about 3 mil-

lion people, is between 3600 m and

4100 m above sea and Cochabamba,

which has about 1 million people is

also at an altitude of 2600 m. Building

the plant at a lower altitude means a

higher output from the gas turbines.”

Termoeléctrica del Sur is located in

southern Bolivia near the border with

Argentina about 120 km east of the

city Tarija, and due to its location

will be able to export power to neigh-

bouring South American nations.

Termoeléctrica de Warnes, is in the

Warnes province next to the city

Santa Cruz; and Termoeléctrica Entre

Ríos is in Cochabamba province,

175 km southeast of Cochabamba.

The overall project has moved at a

relatively fast pace, especially when

considering the logistics of delivering

the equipment from different parts of

the world to three dispersed sites in

Bolivia.

Following nalisation of the Memo-

randum of Understanding (MoU) in

2015, Siemens signed the nal con-

tract and was given Notice-to-Proceed

on May 31, 2016. Siemens’ consor-

tium partner TSK was largely respon-

sible for electrical systems, civil

works, erection and installation.

Manufacture of the gas turbines be-

gan immediately in Finspång, Swe-

den, and the rst unit was ready for

shipping in April 2017.

Manufacturing of the steam tur-

bines, HRSGs as well as the 25 gen-

erators, eight bypass stacks, 25 trans-

formers and the power plant control

systems began on completion of engi-

neering design.

As custom-engineered components,

manufacturing of the boiler and steam

turbines started slightly later than the

gas turbines. Manufacture of the boil-

ers was carried out in China and the

rst was shipped in May 2017. Steam

turbine manufacture was undertaken

in Brazil and the rst machine was

shipped in June 2017.

Shipping and delivery of the major

equipment was quite a challenge,

one that required a great deal of

coordination.

Entfellner said: “We had a team in

Vienna coordinating the engineering,

as well as people in Spain to coordi-

nate the civil works and balance-of-

plant. And of course we had people

working on the gas turbine develop-

ment, boiler design and steam turbine

design, etc. This means we had an

international team to coordinate get-

ting all the equipment ready for ex-

works and getting it to site on time.”

Marcus Koerber, Transport and Lo-

gistics Manager says the project was

“interesting” as well as “challenging

from time-to-time”. Overall there

were about 1000 shipments – all

scheduled to be delivered within a

time frame of roughly one year.

Koerber noted: “We had a lot of

heavy equipment such as the gas

turbines and boiler parts. Some of

the boiler parts weighed up to 170 t

each. And in Bolivia there was a

shortage of the [transport] equip-

ment needed to deliver everything at

the same time. The main task was to

coordinate the shipments in a way so

that equipment was available at the

same time and to arrive at the sites

according to the schedules for erec-

tion and execution.”

The overall project called for ap-

proximately 400 heavy haulage ship-

ments to the three power plants –

nearly 100 heavy-lift shipments and

300 oversize cargo shipments.

In order to streamline deliveries and

have equipment arriving at the same

time to site, Siemens shipped genera-

tors on the same vessel as the gas

Special Project Supplement

THE ENERGY INDUSTRY TIMES - APRIL 2019

Bolivia’s three combined

cycle power plants. From left

to right: Termoeléctrica del

Sur (480 MW); Termoeléctrica

Entre Ríos (480 MW) and

Termoeléctrica de Warnes

(520 MW)

Most of the equipment arrived by boat and was then transported by road to the three sites

THE ENERGY INDUSTRY TIMES - APRIL 2019

Special Project Supplement

Almost all of the equipment

had to be navigated across

the Andes mountains at a

height of 4680 m

Becerra from Ende Andina

says the availability of

electricity will facilitate the

general socio-economic

development of the country

ing of subsequent gas turbine or put-

ting water treatment plants, etc., into

operation is always much quicker.”

Due to the logistical challenges

with transport, buffers of between

three and six months were built into

the agreed schedules to allow for

force majeure.

Entfellner explained: “For example,

in del Sur there is a buffer of three and

a half or four months, and similar for

Warnes; and at Entre Ríos, we have a

buffer of eight months. So for Entre

Ríos, our intention is to handover the

project in October/November but we

are allowed until June next year.”

The additional capacity from all

three sites is scheduled to be fully

available by the end of this year or the

beginning of next year.

In addition to the jobs resulting

from the use of several local compa-

nies during erection, operation and

maintenance of the plants will also

provide jobs for the local communi-

ties. “We have already carried out a

lot of training for operators, who

have been issued with certicates,”

said Entfellner. “We are now doing

on-the-job training for people who

will nally operate the plants.”

He also noted that a Long Term

Service Agreement (LTSA) is already

in place for the existing units and this

will be extended to cover the new

units as well.

Notably, servicing will be carried

out by a new service and training

centre that is being built by Siemens

on a 9200 m

2

site at the Parque Indus-

trial Latinoamericano (PILAT) in the

city of Warnes. The centre will also

function as a hub for servicing power

equipment installed in the South

America region. The service centre

will be complete by November this

year, with the training centre operat-

ing in the rst quarter of next year.

two followed in mid-December and

the plant received its Provisional Ac-

ceptance Certicate in February. The

rst two SGT-800s at Warnes were

ignited in January this year, with the

second two following in late February.

Now just six months after rst ring at

del Sur, commissioning of these two

plants is currently ongoing under the

watchful eye of the commissioning

teams.

At Entre Ríos, commissioning be-

gan recently with back-energising

taking place in March to provide

power from the grid to operate auxil-

iary equipment. The next key mile-

stone will be ring of the gas turbines,

which is expected in early to mid-

April.

Entfellner commented: “The rst

unit is always the most complicated

because there are always some new

competences involved but with les-

sons learned, you can see synchronis-

Tim Frace, Head of Siemens Power

Generation Services Latin America,

said: “The Service Centre is key to

being able to service the large SGT-

800 eet in Bolivia. It will also

eventually become a regional Ser-

vice Centre for the SGT-800 eet.

We will be able to provide remote

monitoring for our SGT-800 technol-

ogy and other units in Bolivia.

Moreover, the service centre will

also work as a training centre for our

customers and personnel.”

Siemens is investing over $23 mil-

lion in the facility, which it says will

improve delivery time on parts, tool-

ing and other resources.

One of the important aspects of the

centre will be an innovation room.

This room will be used to monitor the

performance the entire SGT-800 eet

in Bolivia by using Siemens’ latest

digital technologies and solutions to

diagnose and analysis the data pro-

duced by the eet.

The centre is expected to employ

about 130 people and is predicted to

grow. “The Service Centre will con-

tinue to grow and in order to cover

the needs for this centre, many high

skilled jobs will be generated for

the local communities” said Frace.

“This will help develop more spe-

cialised professionals with interna-

tional certication.”

Certainly, the centre and new plants

will improve living standards quickly.

Some areas of Bolivia have suffered

several power cuts in recent times,

due to demand outstripping supply.

Regarding the importance of this

project Becerra said: “Ende Andina is

part of a development project devised

by the administration of President

Evo Morales in the electricity eld.

It’s going to make the national inter-

connected system highly reliable, and

the availability of electricity means

we will have the tools to facilitate the

general socio-economic development

of the country, thanks to the avail-

ability of a service and a resource

such as electricity.

“It will also trigger the growth of the

electricity network, the national inter-

connected system. Although this ex-

tends to eight of the nine provinces in

Bolivia, there is still huge scope for

integrating users.

“What’s more, another main impact

is the rational and efcient use of gas

as a resource, which is a pillar that

keeps the Bolivian economy going.

It will free-up volumes of gas that

will be used for the industrialisation

that is currently under way on a

grand scale, the industrialisation of

gas, as well as other types of indus-

trialisation, such as agricultural pro-

duction, nished products, etc.”

John Prado, Siemens Country CEO

of Bolivia believes that bringing reli-

able electricity to urban and rural

areas, while improving supply to in-

dustrial sectors, will help the econo-

my to grow. This will in turn present

further opportunities – in Bolivia and

the rest of the region.

“This project also helped Argentina.

Argentinean customers witnessed

what was being implemented in Bo-

livia and wanted the same technology

to benet from the exibility and ef-

ciency it offers. Other countries like

Colombia have also visited the Bo-

livia power plants to adopt similar

models.”

He concluded: “This type of col-

laboration with the government and

other entities is a great model to fol-

low in other regions of the world to

develop and implement electricity

for generations. With our innovative

technologies and our huge project

expertise we improve the quality of

life for people all over the world.”

Electricity for generations:

Fulfilling a country’s vision

A stable power infrastructure ensuring reliable supply of electricity is

indispensable for every economy. Together with our partners we co-create

and fulfill energy concepts for countries and regions elevating their power

supply to a new level.

Since 1990, Siemens has completed over 500 turnkey power plants with

total output exceeding 155,000 megawatts. With the right ideas,

innovations, and know-how, we are the partner of choice for our customers.

By generating reliable electricity for generations we help driving the

socio-economic development of a country – and the future of its people.

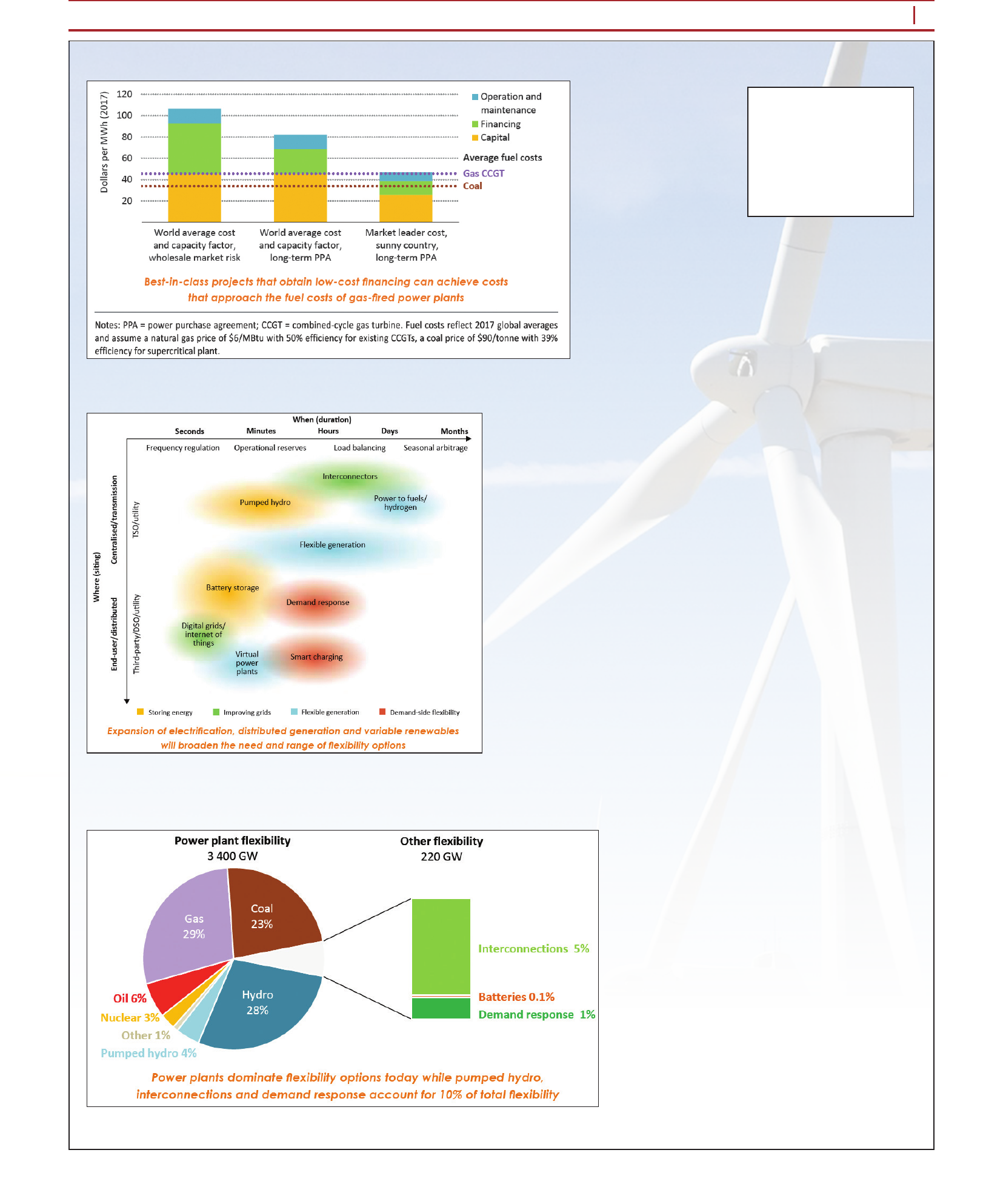

Source: World Energy Outlook 2018

THE ENERGY INDUSTRY TIMES - APRIL 2019

11

Energy Industry Data

Solar PV levelised cost of electricity, 2017

Growing needs and range of options for exibility

Flexibility in the global power system, 2017

World Energy Outlook 2018, © IEA/OECD, Figure 7.15, page 297

World Energy Outlook 2018, © IEA/OECD, Figure 7.20, page 302

World Energy Outlook 2018, © IEA/OECD, Figure 7.19, page 302

For more information, please contact:

International Energy Agency

9, rue de la Fédération

75739 Paris Cedex 15

France.

Email: bookshop@iea.org

website: www.iea.org

THE ENERGY INDUSTRY TIMES - APRIL 2019

13

Industry Perspective

M

ost industries have gone

through revolutionary chang-

es over the last two de-

cades. Blockbuster and Hollywood

Video rental stores were disrupted by

Netix. Retail shopping was inter-

rupted by e-commerce, led by Ama-

zon, followed soon by almost every

brick-and-mortar store. The trans-

portation market is in the process of

being disrupted by Uber and Lyft;

the hotel industry by AirBnb; and the

list of examples goes on.

During these revolutions, some in-

dustries end up with extinction of

traditional players while others see

the dust settle with old players

holding a much smaller market po-

sition. Part of the extinction de-

pends on how fast the incumbents

adopt new technologies and inno-

vate on their own. Intel for years

has followed the philosophy of dis-

rupting its own product before any-

one else does and introduces newer

versions of its microprocessor chips

every year or two, for example.

The energy industry is currently

going through its own disruption cy-

cle. The traditional business model

for regulated utilities has been to

build infrastructure for the genera-

tion, transmission and distribution of

electricity and to earn a rate of return

on capital investments. The public

commissions regulate utility prots

by dening the energy rate that gives

them a specic rate of return on their

investment.

Importantly, what is changing in

the energy industry is the availability

of new technology.

First, the presence of renewable en-

ergy resources like solar gave con-

sumers the option to produce their

own energy, which takes revenue

away from the traditional utility

model. Then came the commerciali-

sation of battery storage technology

at scale funded by electric vehicles,

allowing consumers to store the en-

ergy they produce from renewables.

The net effect is a big dent in the tra-

ditional business model of utilities

since their infrastructure costs are

not reduced in the same proportion

as their revenues. As they are a regu-

latory-protected industry, they are

more immune to external pressures

and the threat of extinction as com-

pared to the other independent, un-

protected industries, but they are not

100 per cent safe.

Also, a new class of technology

companies is looking to address an-

other new phenomenon in energy:

opposite swings on the grid. As more

and more homes produce their own

energy with solar and more electric

vehicles get on the road, the grid has

two opposite load swings. In the US,

California’s landmark mandate that

all new homes built starting in 2020

are required to have solar and an In-

ternational Energy Agency estimated

125-220 million EVs worldwide

coming by 2030 are clear signs of

the direction the industry is headed –

putting immense pressure on a grid

that was never built for this model.

Technologies looking to control de-

vices in the home (or so-called

Smart Home) like smart thermostats

that pre-cool the home during off

peak hours, or consumer technolo-

gies designed to motivate people to

run their major appliances, such as

the dryer or pool pumps, when there

is a surplus on the grid, are signi-

cantly changing the energy supply to

the home. What was once a simple

supply of electrons is becoming a

very complex industry where many

other players outside of utilities have

a say in solving the problems – and

adoption of these means utilities

only own a fraction of total energy

supply, essentially reducing their

market share.

Luckily, not all odds are against

utilities. Technology can also be part

of the solution that presents utilities

with new, innovative ways to meet

external pressures and tackle head-

on the shifting industry dynamics.

One major technological change in

the last decade is the arrival of smart

grid. Smart meters, smart routers and

other equipment have been mod-

ernising the grid for reliable power

and automation. There is a treasure

trove of data produced by smart me-

ters that contains information about

the load in each home. But, it is

locked. Will technology come to res-

cue utilities and unlock this data,

which is the key to understanding

each customer and personalising

utility service?

In the age of big data, where large

cloud servers running extremely

complex algorithms using articial

intelligence (AI) and machine learn-

ing solve big problems, it is abso-

lutely possible to unlock this data.

Technologies like energy disaggre-

gation and lifestyle segmentation al-

low the time series, whole-home

consumption data from smart meters

to be analysed and identify appli-

ance-level energy use without the

need for any sensors in the home.

Large appliances like air condition-

ers, heaters, refrigerators, dryers,

electric vehicles, etc., leave their

electronic “ngerprint” when turned

on and off. But, they are not easily

visible because they are often in use

overlapping with each other and

hard to separate from whole-home

consumption waveforms. AI tech-

nology comes to the rescue and ap-

plies algorithms that have been pre-

trained to separate the signatures.

This is similar to how Facebook or

Google pattern recognition technolo-

gy identies faces in an image, and

once tagged, can even identify

whose face it is automatically in the

future. In other words, AI has

learned to recognise this person. For

utilities, faces are replaced with ap-

pliance recognition. Now that utili-

ties can understand the consumption

behaviours of appliances by type,

time and frequency of use, combined

with all the publicly available demo-

graphic information on homes and

weather, they are in a position to per-

sonalise customer engagement à la

the consumer tech giants.

In what ways are utilities using this

newly found information? For start-

ers, energy bills are becoming ite-

mised – just like mobile phone and

credit card statements are – breaking

down for customers where their

spend is going each month. Next, the

$7.5 billion utilities spend on energy

efciency programmes to fund a va-

riety of rebates (like that on smart

thermostats and LEDs), home up-

grades, appliance replacements (re-

frigerators, pool pumps, etc.), can

now be spent more efciently by tar-

geting customers who would benet

the most. No more sending pool

pump rebates to homes without pools.

Lastly, new business models are

enabled through this customer usage

information. Most utilities are start-

ing to upsell other products and ser-

vices like electric vehicle chargers;

system installations and repairs; and

energy efciency products such as

smart thermostats. In the competitive

selling world where consumers

make decisions by looking at user

ratings on Amazon and Yelp, utilities

were at a disadvantage. With the per-

sonalised information, however,

their ability to not only target the

right customers for right offers but

also show them the return on invest-

ment (ROI) when buying a product

or service from their utility gives

them a selling advantage.

While AI has revolutionised many

industries over the last decade, it is

still relatively a new frontier in the

energy space. The myriad ways in

which AI will redene the landscape

for utilities is unfolding everyday. In

the near future, do not be surprised if

electric utilities reach out to custom-

ers to sell them an electric car or a

solar and energy storage system; a

smart thermostat or new energy ef-

cient refrigerator; a security system

or even a vacation package. Utilities

may not know your internet brows-

ing habits like Amazon and Google,

but they surely have found an alter-

nate way of catching up in the game

of survival.

Abhay Gupta is Founder & CEO of

Bidgely a technology company offer-

ing disaggregation-powered utility

solutions.

In an age where large

cloud servers running

complex algorithms

using articial

intelligence (AI) and

machine learning

solve problems, it is

possible to unlock the

big data produced

by smart meters –

data that contains

information about the

load in each home.

Some believe that

unlocking this data is

key to the survival of

energy companies.

Abhay Gupta

Gupta: The myriad ways in which AI will redene the landscape for utilities is unfolding everyday

Will AI save the utility business?

systems and regulation. It will also be

a challenge for energy storage to re-

duce costs and improve regular access

to clean energy. A new regulatory

framework is needed that can mone-

tise exibility and include battery

storage in different market mecha-

nisms, such as ancillary services.

Recycling materials in batteries will

also be key to ensuring the sustain-

ability of the industry. Recycling

processes for industrial Li-ion batter-

ies remain immature and expensive,

and are not expected to take-off for a

while. While the cost of fully recy-

cling a battery is falling towards €1

per kg (approx. €10/kWh), this is still

approximately three times higher

than what can be expected from sell-

ing the reclaimed materials on the

market.

Additionally, batteries are still too

expensive for households to adopt,

without even counting for battery

pack and balance of plant costs. Ger-

many has achieved success in democ-

ratising access to battery storage

through public funding. Germany

marked its 100 000th home to install

a battery storage system. In the UK,

the total is just a tenth of that number

as subsidies are lower and the case to

increase PV self-generation is less

attractive.

Battery storage represents an excit-

ing opportunity for the energy market

and one that has the potential to radi-

cally reshape power networks and

rapidly accelerate global progress to-

wards a renewable future. However,

swift progress should not be taken for

granted. Its future is dependent on a

complex set of considerations, from

ongoing research and development,

to regulatory frameworks, a new

mindset from commercial providers

and further cost reduction.

The overall case for battery storage

is clear: it will reduce costs, improve

energy security and above all increase

the percentage of renewable energy

sources in the global power mix. The

question now is how to increase the

existing few GWh deployed globally

currently by helping battery storage

enter the mainstream market. A bat-

tery powered energy future will not

create itself: it will take conscious,

co-ordinated efforts across the public

and private sectors to become reality.

Marianne Boust is Expert in Renew-

able Energy Technologies, Energy

Storage and Utilities Transformation,

Capgemini Invent. For further re-

search on the role of battery storage,

read Capgemini’s Solar and storage:

a roadmap for successful utilities.

R

enewable energy sources are

estimated to account for over

30 per cent of the global pow-

er supply by 2040, with this gure

rising to as high as 50 per cent in ad-

vanced markets such as Europe.

Yet if the potential of renewables in

playing a larger role in the global

energy mix is to be achieved and

contribute to a global reduction in

carbon emissions, several technologi-

cal barriers must be overcome. Chief

among these is the challenge of

matching renewable energy supply

with consumer demand and xing the

intermittency of solar and wind en-

ergy sources. How can power supply

be rendered reliable, even when the

sun isn’t shining and the wind is not

blowing?

Recent improvements in battery

technology offer hope of a compre-

hensive answer to this problem. If

energy generated from intermittent

sources can be stored cost-effectively

and at scale, one of the primary fac-

tors holding back renewable energy

development will have been resolved.

As such, while the renewable energy

debate has long been focused on

competing means of supply, the cost

and capacity of storage is now fast

rising up the agenda. Over $600 bil-

lion of investment into energy storage

is expected between 2018 and 2040,

according to ndings from Bloom-

berg NEF. This is already taking ef-

fect. In the United States, utilities are

investing in grid-scale storage rather

than building new power plants. Over

2018, battery storage grew by 27 per

cent, with 431 MWh installed. US

storage capacity is expected to triple

in 2019 to 1233 MWh.

Acquisitions, including Shell’s re-

cent purchases of Sonnen and Lime-

jump, also indicate a market that is

turning its attention to batteries and

energy management solutions.

As batteries start to play an active

role in national energy infrastructure,

the role of batteries in powering the

renewable revolution is shifting from

concept to reality. That in turn raises

questions over what happens next,

and how developments to date can be

catalysed into meaningful, long-term

progress.

Batteries are attracting increasing

investment and interest for a number

of reasons, the rst of which is their

versatility regarding the number of

possible applications across the ener-

gy supply chain. Batteries have a role

to play both at grid-scale, plugging

gaps and creating exibility in critical

energy infrastructure, and behind the

meter, giving individual enterprises

and households more control over

their renewable energy supply.

Secondly, the cost of battery storage

has been reducing rapidly, down ve-

fold over a decade, and is expected to

continue falling. From $200/kWh in

2017, the cost of a battery cell is ex-

pected to decrease another 66 per cent

by 2030, according to Capgemini’s

‘World Energy Market Observatory’

report.

Thirdly, we are approaching a tech-

nological breakthrough that would

transform the potential of battery

storage. Currently, most battery stor-

age relies on the lithium ion model

that was developed in the 1980s. Over

the last decade, strides have been

taken towards the development of

solid state batteries, which replace the

liquid electrolyte that facilitates con-

duction within lithium ion models

with a comparable solid.

This allows for improved energy

density, increasing the storage poten-

tial of each battery at the same time as

reducing its weight, and ultimately

bringing down its cost further. Solid

state batteries will also be able to

charge more quickly, and require

charging less frequently. And, by re-

placing a ammable liquid for a solid,

there is potential for safety to be im-

proved too. The solid state battery’s

increased tolerance for heat will obvi-

ate the need for cooling systems that

add both bulk and cost.

Manufacturers vary on how soon

the solid state battery will be ready for

use, with Panasonic and Toyota

among those warning that it cannot be

expected to enter the mainstream for

another decade. But the prospect of

such a signicant breakthrough, on

top of the already notable progress

made on cost and capacity with exist-

ing technology, points towards a

market that will before long have

storage of renewable energy as its

fulcrum. So what’s next for an indus-

try that can see its future, but can’t yet

access the technology that would re-

alise the vision?

In recent years, developments in

battery technology have largely been

led by Asian battery manufacturers

seeking to unlock the electric vehicle

(EV) market. Players such as Pana-

sonic and BYD have been competing

to develop the battery that will keep

an EV on the road for the longest time

between charges at the lowest cost.

That has led to a benecial spill over

effect on the energy market and a

slow take-off of the EV market, with

Tesla leading a project to create the

world’s largest lithium ion battery in

South Australia, an area which has

been consistently affected by extreme

weather and blackouts. The installa-

tion has a storage capacity of 129

MWh. In its rst year it delivered cost

savings estimated at $40 million, and

contributed to improved grid security

in the aftermath of a major lightning

strike. Similar projects are now under

way, as a keystone of the South Aus-

tralian government’s target to source

100 per cent of power from renewable

sources by 2025.

Now the wider industry is starting to

follow, and both carmakers and utili-

ties are jumping in. Utilities are up-

ping their investments in energy

storage, with the UK’s ScottishPower

recently announcing a £2 billion in-

vestment programme. In Germany,

Volkswagen recently partnered with

the battery production startup North-

volt, to create a new consortium to

advance batteries for EVs in Europe.

For that potential to be realised,

some challenges must be addressed.

Primarily, there is a mismatch be-

tween the design of current energy

THE ENERGY INDUSTRY TIMES - APRIL 2019

Energy Outlook

14

The case for battery storage is clear: it will reduce costs, improve energy security and above

all increase the percentage of renewable energy sources in the global power mix. The

question is how to increase global deployment. Marianne Boust

A battery-powered

renewable future

Boust: there is a mismatch between the design of current

energy systems and regulation